Let’s be direct: when an insurance company offers you a fraction of what your claim is worth, it’s rarely an honest mistake. It’s often a calculated business strategy designed to protect their profits at your expense. This is the reality of an underpaid commercial property claim. Insurers often count on you being too overwhelmed to question their assessment or too confused by the policy’s fine print to fight back. But you don’t have to play their game. Understanding their tactics is the first step to defeating them. This article will expose the common reasons claims are underpaid and give you a clear plan to demand more.

Key Takeaways

- Challenge the insurer’s numbers: An insurance company’s initial offer is often based on an incomplete inspection or lowball estimates. Counter their assessment by getting detailed, independent repair quotes from local Texas contractors to show the true cost of recovery.

- Documentation is your most powerful tool: A strong dispute requires strong evidence. Meticulously collect photos, receipts, contractor estimates, and a log of every conversation to build a solid case that proves the full value of your claim.

- You have legal options against unfair tactics: If your insurer refuses to pay what you are owed, you do not have to accept it. Texas law allows you to hold them accountable, and a property insurance attorney can help you file a formal dispute or a bad faith lawsuit.

What Is an Underpaid Commercial Property Claim?

An underpaid commercial property claim is exactly what it sounds like: your insurance company offers you a settlement that’s far less than what your claim is actually worth. After paying your premiums and holding up your end of the deal, you expect your insurer to do the same when disaster strikes. But when their payout doesn’t even begin to cover the cost of repairs, inventory replacement, and other losses, it can put your entire business in a tough spot.

This situation is frustratingly common for Texas business owners. You’re left with a check that won’t make you whole and a long road to recovery. The insurer might have approved a portion of your claim, but the amount is simply not enough to get your business back on its feet. Understanding that you don’t have to accept this first offer is the first step. A property insurance lawyer can help you determine what your claim is truly worth and fight for the full compensation you deserve.

Common Reasons Your Claim Might Be Underpaid

So, why does this happen? An insurer might underpay your claim for several reasons, and it’s rarely a simple mistake. Some of the most common tactics include providing repair estimates that don’t reflect local labor and material costs, or disputing the extent of the damage your property actually sustained.

They might also incorrectly apply policy exclusions to limit their payout, overlook or misclassify damaged business items, or let processing delays cause even more damage that they then refuse to cover. Sometimes, the policy language itself is so confusing that it leads to disagreements about what’s actually covered. These issues can quickly turn a straightforward claim into a complex dispute.

Underpaid vs. Denied: What’s the Difference?

It’s important to know the difference between an underpaid claim and a denied claim, as your next steps will be different for each. An underpayment of a claim means the insurance company agrees your loss is covered and makes a payment, but the amount is less than what you need or what your policy promises. You get a check, but it’s not enough.

A denied claim, on the other hand, is an outright refusal to pay. The insurer is stating that your loss is not covered by the policy at all. While both situations are difficult, an underpaid claim acknowledges the validity of your loss, which can be a very different starting point for a dispute.

Why Do Insurance Companies Underpay Claims?

After you file a claim, you expect your insurance company to hold up its end of the bargain. Unfortunately, that doesn’t always happen. Insurance companies are for-profit businesses, and their goal is to protect their bottom line. This can create a conflict of interest where paying you less means more profit for them. While not every low offer is a sign of bad faith, many underpayment tactics are intentional strategies used to minimize payouts. Understanding these common reasons can help you spot when your insurer isn’t treating you fairly.

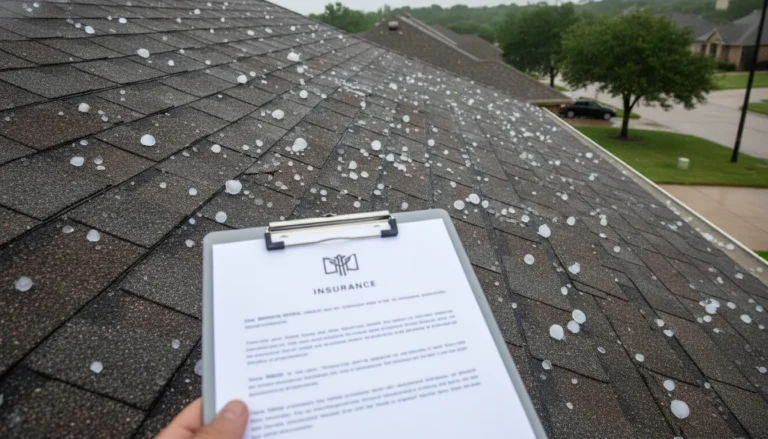

Using Lowball Estimates and Incomplete Inspections

One of the most common ways insurers underpay claims is by starting with a lowball repair estimate. The adjuster sent by your insurance company works for them, not you. They may conduct a quick, incomplete inspection that misses hidden damage, like water saturation behind walls or subtle structural issues from a storm. Their estimate might also rely on outdated pricing for materials and labor, failing to account for the current costs in Texas, which often spike after a major weather event. This results in an offer that doesn’t come close to covering the actual cost of restoring your property.

Misinterpreting Your Policy’s Fine Print

Insurance policies are notoriously complex legal documents filled with dense language and specific exclusions. Insurers can take advantage of this complexity. They might interpret ambiguous terms in their favor or incorrectly apply an exclusion to deny coverage for part of your damages. For example, they could argue that damage from wind-driven rain isn’t covered under your policy, even when it should be. When an insurer uses the fine print against you, it’s a clear sign you need an expert to review your policy and advocate for your rights as a policyholder.

Undervaluing Your Property’s Replacement Cost

A commercial property claim isn’t just about the building; it also includes everything inside it. This can be your inventory, specialized equipment, office furniture, and computers. Insurers often undervalue these items by applying excessive depreciation or simply leaving things off the list, especially if your documentation isn’t perfect. They might offer the actual cash value (the depreciated price) when your policy covers the full replacement cost. For a business, this discrepancy can be devastating, leaving you without the funds needed to replace essential assets and get back to work.

Letting Delays Worsen the Damage

Sometimes, an insurer’s most effective tactic is simply to wait. Unreasonable delays in inspecting your property or processing your claim aren’t just frustrating; they can cause the damage to get much worse. A small roof leak can lead to widespread mold growth and structural rot if it isn’t addressed quickly. The insurer might then turn around and refuse to pay for this secondary damage, arguing you failed to mitigate your losses. These intentional delays are a serious issue and can be a form of insurance bad faith, which is why it’s so important to have a Fort Worth property insurance lawyer on your side.

How Can You Tell if Your Claim Was Underpaid?

After you file a claim, it’s easy to feel relieved when the insurance company sends a check. But just because a claim settles without a fight doesn’t mean the payment was fair. Many business owners accept the first offer they receive, not realizing it’s far less than what they’re actually owed. The key is to know the warning signs and understand how to verify that the settlement offer truly covers the full extent of your losses. Being proactive can make the difference between a partial recovery and getting the full amount you need to rebuild.

Red Flags of an Underpaid Claim

An underpaid claim often starts with an offer that feels rushed or suspiciously low. If the insurance adjuster’s estimate is drastically different from the quotes you’ve received from local contractors, that’s a major red flag. Pay close attention to the adjuster’s reasoning. They might use vague policy language or apply exclusions too broadly to justify the low number. Another warning sign is pressure to cash the check and sign a release quickly. A fair offer should fully account for all your documented damages, so if the amount doesn’t cover everything from structural repairs to replacing inventory, it’s time to ask more questions. A Fort Worth property insurance lawyer can help you identify these tactics.

Get an Independent Damage Assessment

The adjuster sent by your insurance company works for them, not for you. Their goal is often to minimize the payout. If you suspect their assessment is incomplete or inaccurate, your best move is to get a second opinion. You can hire a public adjuster, who works on your behalf, or bring in a trusted, independent contractor to provide a detailed, line-by-line estimate for the repairs. This independent assessment gives you a powerful tool for comparison and negotiation. It replaces the insurer’s lowball number with a realistic figure based on local material and labor costs, creating the strong documentation you need to challenge an unfair offer.

Review Your Policy and All Documentation

Your insurance policy is a contract, and it’s the ultimate guide to what you are owed. Take the time to read through it carefully, paying special attention to your coverage limits, deductibles, and any specific clauses related to your type of damage. It can be difficult for someone who isn’t an expert to find everything a policy covers, but understanding the basics is your first line of defense. Compare the insurer’s settlement breakdown against your policy terms and your own documentation. Having a complete file with photos, videos, repair quotes, and a detailed inventory of damaged items will give you the evidence needed to prove the true value of your claim.

What to Do When Your Commercial Property Claim Is Underpaid

Receiving a settlement offer that barely covers your damages can feel like a second disaster. But an underpayment isn’t the end of the road. You have the right to challenge the insurance company’s decision and fight for the full amount you need to recover. Taking a structured, evidence-based approach is the key to turning the tables. Here are the steps you can take to build a strong case and demand a fair payment.

Document Everything

Your first and most important job is to become a meticulous record-keeper. Many claims are underpaid simply because the business owner doesn’t provide enough strong paperwork to justify a higher amount. Start by gathering every piece of information related to your property and the damage. This includes pre-loss photos, post-loss photos and videos, receipts for any temporary repairs, and a log of every conversation with your insurer. Note the date, time, and who you spoke with. Keep copies of your policy, the adjuster’s report, and any written correspondence. This detailed file is the foundation of your dispute and your most powerful tool in negotiations.

Get Professional Repair Estimates

Don’t just accept the estimate provided by the insurance company’s preferred contractor. Their goal is often to keep costs low for the insurer, not to ensure your property is fully restored. Instead, get your own independent repair estimates from at least two or three reputable, local Texas contractors. Ask them for detailed, itemized quotes that break down the costs of both labor and materials. These professional estimates provide a realistic benchmark for your repair costs and serve as concrete evidence to challenge a low offer. Submitting your own estimates shows the insurer you’ve done your homework and won’t accept an unfair valuation.

Consider Hiring a Public Adjuster

If you feel overwhelmed by the claims process, a public adjuster can be a valuable ally. Unlike the adjuster sent by your insurance company, a public adjuster works directly for you, the policyholder. They are experts in assessing property damage, interpreting complex insurance policies, and negotiating with carriers to secure a fair settlement. They manage the entire claims process on your behalf, from documenting the loss to meeting with the insurance company. Public adjusters typically work on a contingency fee, meaning they receive a percentage of the final settlement, so they are motivated to get you the best possible outcome.

Challenge the Insurer’s Assessment

Once you have your documentation and independent estimates in hand, it’s time to formally challenge the insurer’s low offer. You have the right to fight for the full amount you are owed under your policy. Start by writing a clear, professional letter to your insurance company. In the letter, state that you are disputing their settlement amount and explain why you believe it is inadequate. Reference specific line items from your independent estimates and attach copies of all your supporting evidence, including photos and receipts. This creates a formal record of your dispute and forces the insurer to justify their position.

File a Formal Appeal

If your initial challenge doesn’t result in a better offer, the next step is to file a formal appeal. Your insurance policy should outline the specific steps for the company’s internal appeals process. This usually involves submitting another formal letter and all your evidence for review by a different department or a senior claims manager. Following the official process is crucial. If the appeal is still unsuccessful, you haven’t run out of options. At this stage, it often becomes necessary to explore your legal rights, as an experienced attorney can address the complex property insurance disputes that insurers are unwilling to resolve fairly.

What Are Your Legal Options for an Underpaid Claim?

If you’ve challenged your insurer’s low offer and still hit a wall, it might be time to explore your legal options. Your insurance policy is a contract, and when the insurance company doesn’t hold up its end of the deal, you don’t have to accept it. Texas law provides strong protections for policyholders, giving you the power to hold your insurer accountable and demand the full and fair payment you deserve for your commercial property damage.

When to Call a Property Insurance Attorney

When your attempts to negotiate a fair settlement are ignored or dismissed, it’s a clear sign to call a professional. You have the right to fight for the full amount you are owed, and a property insurance lawyer can be your strongest advocate. These attorneys understand the complex language of insurance policies and the tactics carriers use to minimize payouts. They can take over communication with the insurer, build a strong case with compelling evidence, and represent your best interests. An experienced attorney levels the playing field, showing the insurance company that you are serious about getting the compensation needed to repair your property.

Filing a Bad Faith Insurance Claim in Texas

Sometimes, an underpaid claim isn’t just a disagreement over repair costs; it’s a result of the insurer acting in bad faith. This happens when an insurance company unreasonably delays, underpays, or denies a claim without a valid reason. Taking your insurer to court for bad faith can force them to pay the full amount of your damages. You might also recover money for extra costs you incurred because of their delay, and even for the emotional stress they caused. A successful bad faith lawsuit can result in the insurance company paying what they originally owed plus interest, attorney fees, and additional penalties for their misconduct.

Know Your Rights and Deadlines

As a policyholder in Texas, you have rights. Your insurance company has a legal duty to pay valid claims as long as you’ve paid your premiums and met your obligations under the policy. They must also act in a timely manner, which means they have to respond quickly and reasonably to your communications about a claim. Texas has specific laws that set deadlines for insurers to acknowledge, investigate, and pay claims. It’s also important to know that you have a limited time to file a lawsuit. An experienced attorney like Tim Hoch can help you understand these critical deadlines and protect your right to take legal action.

Related Articles

- Commercial Property Insurance Claims Attorney | Hoch Law Firm, PC

- When to Hire a Fort Worth Underpaid Commercial Claim Attorney

- 5 Signs You Need an Apartment Complex Insurance Claim Lawyer

- How a Denton Business Property Damage Lawyer Helps You

- When to Hire a Hurricane Damage Insurance Lawyer

Frequently Asked Questions

What’s the difference between a public adjuster and a property insurance lawyer? Think of it this way: a public adjuster is an expert on the damage, while a lawyer is an expert on your legal rights. A public adjuster is great at assessing the full scope of your property loss and negotiating with the insurance company for a higher settlement based on that evidence. A lawyer steps in when the insurer disputes your claim unfairly, acts in bad faith, or refuses to negotiate. If your case needs to go to court, you will need a lawyer to represent you.

What if I already cashed the settlement check? Is it too late to dispute the amount? Cashing a check can complicate your situation, but it doesn’t automatically close the door on your claim. It often depends on whether you signed a “full and final release” document along with it. Even if you did, you may still have options. The most important thing is to stop all communication with the insurer and speak with a property insurance attorney immediately to understand your specific rights and next steps.

My insurer is taking forever to process my claim. Is there anything I can do? Yes, you can and should take action. In Texas, insurance companies are required to handle claims in a timely manner. Unreasonable delays can be a form of insurance bad faith, especially if the delay causes more damage to your property. Keep a detailed log of all your communications and send a formal letter requesting an update on your claim’s status. If the delays continue, it is a strong signal that you need legal advice.

How much will it cost to hire an attorney for my underpaid claim? This is a common worry, but getting legal help is more accessible than you might think. Most experienced property insurance lawyers, including Hoch Law Firm, work on a contingent fee basis. This means you don’t pay any attorney’s fees upfront. The law firm only gets paid if they successfully recover money for you through a settlement or a court verdict.

Should I accept the insurer’s preferred contractor for repairs? It’s generally best to find your own independent contractor. The contractors recommended by your insurance company have a relationship with the insurer, and their main goal may be to complete the job for the lowest possible cost, not necessarily to the highest standard. Getting estimates from your own trusted, local contractors ensures the quote reflects the true cost of restoring your property correctly.