A claim denial isn’t just a business problem; it’s a personal one that brings immense stress while you’re already trying to manage a damaged property. It’s easy to feel like you’re facing a corporate giant alone. The good news is that you don’t have to accept their decision without a fight. Taking the right steps immediately after receiving a denial can dramatically change the outcome. Instead of letting frustration take over, you can channel that energy into a methodical response. This article is your playbook for what to do if your commercial property claim is denied, outlining the practical steps to take to regain control and effectively pursue the compensation your business deserves.

Key Takeaways

- Documentation is your best defense: Keep detailed records of your property’s condition before a loss occurs. After damage, document every detail of the incident and all communication with your insurer to build a powerful, evidence-based case.

- A denial is an opening, not an ending: Don’t accept an insurer’s “no” at face value. Scrutinize the denial letter, gather your own independent repair estimates, and construct a formal appeal that systematically counters their reasoning.

- Know when to call for backup: If your business faces significant losses, the policy is confusing, or the insurer is stalling, it’s time to consult an attorney. A legal professional can hold the insurance company accountable and fight for the full value of your claim.

Why Insurers Deny Commercial Property Claims

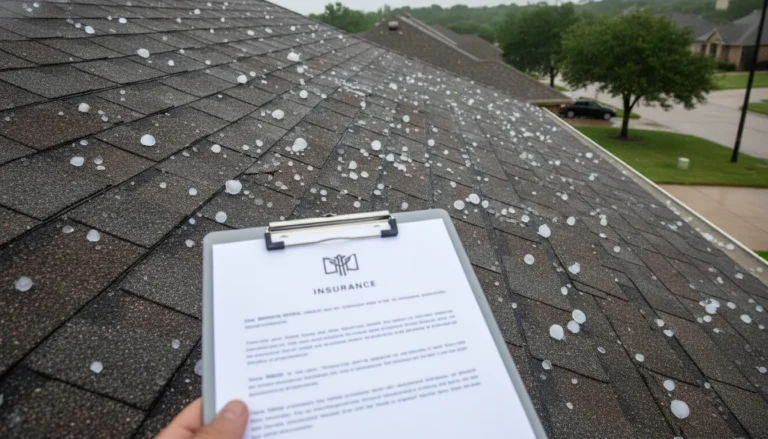

Receiving a denial letter after filing a commercial property claim can feel like a gut punch. You’ve paid your premiums faithfully, and now, when you need support the most, the insurance company is refusing to help. It’s important to understand that a denial isn’t always the final word. Insurance companies are businesses focused on their bottom line, and sometimes, denying a valid claim is part of their strategy. These denials often fall into a few common categories, from citing confusing policy language to questioning the cause of the damage itself. Knowing why your claim was denied is the first step toward fighting back.

Hidden Policy Exclusions

Commercial insurance policies are notoriously complex, often filled with dense legal jargon and specific exclusions. An insurer might deny your claim by pointing to one of these hidden clauses. They may argue that the specific type of damage you suffered isn’t covered, or that a particular condition wasn’t met. Because insurance companies often use confusing policy rules to pay less or deny claims, it can be difficult for a business owner to argue against their interpretation. This is a common tactic used to protect their profits, leaving you to sort through a complicated document while your business suffers. An experienced property insurance lawyer can help interpret this language and determine if the exclusion is being applied fairly.

Disputes Over the Cause of Damage

One of the most frequent reasons for denial is a disagreement over what actually caused the damage. Your insurer might claim the loss resulted from a non-covered event. For example, after a major storm, they might argue that your roof damage was not from hail but from simple “wear and tear” or old age. They could also blame poor upkeep or a pre-existing issue that your policy doesn’t cover. By shifting the narrative around the cause, the insurance company attempts to move the event from a covered peril to an uncovered one. This frees them from the responsibility of paying the claim, even when the damage is legitimate and should be covered under your Texas policy.

Insufficient Proof of Loss

When you file a claim, the burden is on you to prove the extent of your damages. Insurers have strict requirements for documentation, and if you don’t provide enough evidence, they can use it as a reason for denial. This is known as an “insufficient proof of loss.” This could mean you didn’t submit enough photos of the damage, couldn’t produce receipts for lost inventory, or failed to fill out a form correctly. Even a small oversight in your paperwork can be used as an excuse to delay or deny your entire claim. This makes meticulous record-keeping absolutely essential from the moment a loss occurs, as the insurance company will look for any reason to invalidate your submission.

Claims of Poor Maintenance

In some cases, the insurance company will try to turn the tables and blame you for the damage. They might argue that the loss only happened because you failed to properly maintain your property. For instance, if a pipe bursts and causes water damage, the insurer could allege that you neglected routine plumbing inspections. This strategy attempts to pin the damage on your supposed negligence rather than a covered event. It’s a way for them to avoid their obligations by claiming you didn’t uphold your end of the deal, even when that isn’t the case. You can find more information about protecting your rights on our Justice Blog.

What to Do Immediately After a Denial

Receiving a denial letter can feel like a final verdict, but it’s often just the start of a conversation. Your insurance company has made its decision, but you have the right to challenge it. Taking the right steps immediately after a denial is crucial for protecting your rights and setting up a successful appeal. Don’t let frustration or disappointment lead to inaction. Instead, channel that energy into a methodical, organized response. By treating the denial as a hurdle, not a roadblock, you can begin building a strong case to get the coverage you deserve for your business.

Review the Denial Letter

Your first move is to read the denial letter, and I mean really read it. This document is your roadmap. The insurance company is required to explain why it denied your claim, and it will often cite specific language from your policy. Carefully check the letter to understand the exact reasons provided, whether it’s a hidden exclusion, a dispute over the cause of damage, or a claim of insufficient documentation. Pay close attention to any deadlines mentioned for filing an appeal. This letter contains the arguments you’ll need to counter, so understanding it completely is the critical first step in fighting back.

Request Your Full Claim File

If the denial letter feels vague or the reasoning doesn’t add up, your next step is to request a complete copy of your claim file from the insurer. This file contains every document related to your claim, including adjuster notes, internal emails, expert reports, and correspondence. It gives you a behind-the-scenes look at how the company handled your case and can reveal inconsistencies or errors in their evaluation. A written request is best for documentation purposes. Getting this file is essential for understanding the full picture and is a key part of our firm’s property insurance claim representation.

Document Everything

Now is the time to become a meticulous record-keeper. Gather every piece of paper and digital file related to your property damage and your claim. This includes your full insurance policy, all communication with the insurer, photos and videos of the damage (before and after any temporary repairs), independent repair estimates, and receipts for any out-of-pocket expenses. Organize everything into a single, accessible file. This collection of evidence is the foundation of your appeal. Strong documentation makes it difficult for an insurance company to argue with the facts of your case and demonstrates that you are prepared to defend your claim.

Pause Any Permanent Repairs

It’s tempting to want to fix everything and get your business back to normal right away, but you should hold off on any major, permanent repairs. Unless it’s an emergency repair needed to prevent further damage, like putting a tarp on a leaking roof, wait. Starting permanent work before the claim is resolved can compromise your case. The insurance company could argue that you’ve destroyed evidence, making it impossible for them to verify the full extent of the original damage. If you must make emergency repairs, document the situation thoroughly with photos and receipts before, during, and after the work is done.

How to Build a Strong Case for an Appeal

Receiving a denial letter can feel like hitting a brick wall, but it’s rarely the end of the road. The key to turning a “no” into a “yes” is to build a powerful, evidence-based appeal that leaves no room for doubt. This means shifting from simply reporting the damage to proving your case with meticulous documentation. By systematically gathering the right information, you can effectively challenge the insurer’s decision and demonstrate the true value of your claim. Let’s walk through the essential steps to construct a solid foundation for your appeal.

Gather Your Policy and Claim Paperwork

Your first move is to become an expert on your own claim. Start with the denial letter; it’s your roadmap. It outlines the exact reasons the insurance company used to deny your claim, often referencing specific clauses in your policy. Next, pull out your complete insurance policy and locate those exact sections. Understanding the insurer’s argument is the only way to build a strong counter-argument. You should also have a copy of your entire claim file, which includes the adjuster’s notes, reports, and all correspondence. Having all this paperwork organized in one place is the critical first step in handling property insurance disputes.

Get Independent Repair Estimates

The insurance adjuster’s estimate is just their opinion of the repair costs, and it’s often a low one. To counter this, you need professional opinions of your own. Reach out to at least two reputable, independent contractors in Texas and ask for detailed, itemized repair estimates. These documents should break down the specific costs for both labor and materials needed to restore your property to its pre-loss condition. This independent documentation is one of your most powerful tools for challenging an underpayment or a denial based on disputed costs. It replaces the insurer’s lowball number with a realistic assessment from experts in the field.

Collect Photo and Video Evidence

Visual evidence makes your damages real and difficult to dispute. If you took photos and videos immediately after the incident, gather them all together. The more comprehensive, the better. Your goal is to create a clear visual record of the full extent of the damage before any cleanup or repairs began. If you have any “before” photos of your property, they can be incredibly helpful for comparison. Organize these files chronologically and add brief descriptions to explain what each image or video shows. This collection of evidence will support your repair estimates and provide undeniable proof of your losses.

Keep a Detailed Communication Log

From this point forward, document every single interaction you have with the insurance company. Create a log to track every phone call, noting the date, time, the name of the person you spoke with, and a summary of the conversation. Save every email and piece of mail you send and receive. This detailed record serves two important functions. First, it keeps you organized and ensures no detail falls through the cracks. Second, it creates a clear timeline of the insurer’s actions. If they stall, provide conflicting information, or are unresponsive, your log becomes powerful evidence of bad faith.

How to Appeal a Denied Claim in Texas

Receiving a denial letter for your commercial property claim can feel defeating, but it isn’t the final word. In Texas, you have the right to challenge an insurer’s decision. The key is to approach it strategically by building a compelling case to formally appeal the denial. This means presenting your evidence in a clear, structured way and understanding the different avenues available to you. Here are the steps you can take to fight for the coverage you deserve.

Write a Formal Appeal Letter

Your first step is to write a formal appeal letter that clearly explains why you believe the denial is incorrect. This letter should be professional, organized, and based on facts. Reference specific sections of your policy that support your claim and attach all your evidence, including photos, independent estimates, and expert reports. Clearly state what you want the insurance company to do, whether it’s reconsidering the claim or covering a specific amount. A well-written letter shows the insurer you are serious about these property insurance disputes.

Submit Your Appeal on Time

Don’t let a simple calendar mistake derail your efforts. Your denial letter or policy should specify a deadline for submitting an appeal, and missing it can unfortunately disqualify your case. Treat this deadline as non-negotiable. To create a solid paper trail, send your appeal letter and all documents via certified mail with a return receipt requested. This gives you undeniable proof that the insurance company received your package on a specific date, protecting your right to have your case reviewed. Be sure to keep copies of everything you send for your own records.

File a Complaint with the Texas Department of Insurance (TDI)

If your direct appeal doesn’t work, don’t lose hope. Your next move can be to file a complaint with the Texas Department of Insurance (TDI). The TDI is the state agency that regulates insurers and protects consumers. They can investigate your complaint and mediate with the company on your behalf. While they can’t force an insurer to pay, their involvement often prompts a more serious review of your claim. You can learn how to file a formal complaint on their website or call their Help Line at 800-252-3439 for guidance.

Explore Mediation and Appraisal Options

Sometimes, the dispute isn’t about whether the damage is covered, but how much it will cost to fix. In these cases, your policy may include provisions for mediation or appraisal. Mediation involves a neutral third party who helps you and your insurer negotiate a settlement. Appraisal is a process where each side hires an independent appraiser to value the loss, and an umpire resolves any differences. Both can be effective ways to settle disagreements without the time and expense of a lawsuit. Check your policy documents to see if these options are available to you.

When to Hire a Property Insurance Lawyer

Navigating a denied property claim on your own can feel like an uphill battle. While you can manage minor issues directly with your insurer, certain situations are clear signals that it’s time to bring in a legal professional. An experienced attorney can level the playing field and advocate for the full compensation you deserve. If you find yourself in any of the following scenarios, consider it a sign to seek legal advice.

The Insurance Company Is Stalling or Unfair

Insurance companies are businesses, and their goal is to protect their bottom line. This can sometimes lead to them using tactics like unnecessary delays, repeated requests for the same information, or lowball settlement offers. They might use confusing policy language or suggest you were at fault to justify paying less or denying your claim altogether. If you feel your insurer is not acting in good faith or is dragging its feet, a property insurance lawyer can step in to hold them accountable and ensure your claim is handled fairly and promptly.

Your Business Losses Are Substantial

When a commercial property claim is denied or underpaid, the consequences can be devastating. The financial strain can halt your operations, lead to lost revenue, and create immense stress. If the damage to your property is significant and threatens your business’s survival, the stakes are too high to go it alone. An attorney experienced in complex property litigation understands how to calculate and fight for the full scope of your losses, including business interruption costs, so you can focus on getting back to work.

The Policy Language Is Confusing

Insurance policies are dense legal documents filled with technical jargon, exclusions, and conditions that can be difficult for anyone without a legal background to understand. Insurers often deny claims based on their specific interpretation of a clause or a small technicality. If your denial letter cites a policy provision you don’t understand, it’s wise to consult an attorney. A skilled lawyer like Tim Hoch can interpret the contract, challenge the insurer’s reading of the policy, and build a case based on the facts and the law.

Your Initial Appeal Failed

Receiving a denial on your appeal can be disheartening, but it doesn’t have to be the final word. A failed appeal is often the point where legal representation becomes crucial. An attorney can review your entire claim file, identify weaknesses in the insurer’s position, and explore further options like mediation, appraisal, or filing a lawsuit. Having a lawyer with a proven track record of successful results shows the insurance company you are serious about pursuing your claim and are prepared to take the fight to the next level.

How to Prevent Future Claim Denials

Dealing with a denied claim is frustrating, but you can take steps now to strengthen your position for any future claims. While you can’t stop a storm from hitting, you can control how prepared you are for the aftermath. Being proactive is your best defense against an insurance company looking for reasons to underpay or deny your claim. By focusing on your policy, your records, and your responsibilities, you can build a solid foundation that makes it much harder for an insurer to dispute a legitimate loss.

Review Your Insurance Policy Annually

Think of your insurance policy as a contract. You wouldn’t sign a business contract without reading it, and your insurance policy deserves the same attention. Insurers sometimes use confusing policy language or hidden exclusions to deny claims, so understanding your coverage is critical. Make it a yearly habit to sit down and read through your policy, especially when it’s up for renewal. Pay close attention to what’s covered, what’s excluded, and what your coverage limits are. If the language feels overwhelming, a Fort Worth property insurance lawyer can help you understand exactly what you’re protected against before you ever need to file a claim.

Keep Excellent Property Records

When you file a claim, the burden of proof is on you. This is where meticulous record-keeping becomes your most powerful tool. Before any damage occurs, create a comprehensive file for your property. This should include photos and videos of the building’s interior and exterior, maintenance logs, invoices for repairs or upgrades, and any other documents that show the property’s condition. Good records help prevent arguments later by establishing a clear baseline of your property’s value and state before the loss. This documentation is crucial across many types of property damage claims and makes it difficult for an insurer to argue that the damage was pre-existing or resulted from poor maintenance.

Understand Your Duties After a Loss

After your property is damaged, your policy requires you to take specific actions. One of the most important is your duty to mitigate damages, which means you must take reasonable steps to prevent the situation from getting worse. For example, this could involve placing a tarp over a damaged roof to stop leaks or boarding up a broken window to secure the property. Failing to do so can give your insurer a reason to deny your claim. Be sure to document every step you take to mitigate further damage with photos, videos, and receipts for any materials you purchase. You can find more guidance on navigating the claims process on our Justice Blog.

Related Articles

- Business Hail Damage Claim Denied? What to Do Next

- Denied Commercial Property Claim? Your Next Steps

- Commercial Hurricane Damage Claim Denied? Your Next Steps

- Commercial Property Insurance Claims Attorney | Hoch Law Firm, PC

- How a Commercial Insurance Claim Denial Lawyer Can Help

Frequently Asked Questions

What is the most important document to focus on after my claim is denied? Your denial letter is the most critical piece of paper you have. It’s the insurance company’s official explanation for their decision, and they are required to state their reasons. Read it carefully to understand exactly which policy clauses they are using to justify the denial. This letter is your roadmap for building an appeal because it tells you precisely which arguments you need to counter with your own evidence.

My insurer says my storm damage is just “wear and tear.” How do I prove them wrong? This is a very common tactic used to avoid paying for legitimate storm damage, especially for roofs. The best way to fight back is with documentation. Your own evidence, such as records of regular maintenance, photos of your property from before the storm, and a detailed report from an independent contractor or public adjuster, can effectively challenge their assessment. These expert opinions can confirm that the damage was caused by a specific event, like hail, not gradual deterioration.

Can I start making repairs while I’m appealing the denial? You should only make temporary, emergency repairs that are necessary to prevent further damage. For example, you can put a tarp on a leaking roof or board up a broken window. Be sure to take photos and keep receipts for this work. You should hold off on any permanent repairs, because the insurance company could argue that you destroyed evidence they needed to see. Waiting ensures that the full extent of the original damage remains clear throughout the appeal process.

Is it worth hiring a lawyer if my claim isn’t huge, but the denial is hurting my business? Absolutely. The value of legal help isn’t just about the dollar amount of the claim; it’s about holding the insurance company accountable to the policy you paid for. If an insurer is treating you unfairly on a smaller claim, it’s a sign of how they do business. An attorney can step in to show them you are serious, handle the communication, and fight to get the funds you need to get your business back on track, regardless of the claim’s size.

What happens if my appeal is also denied? Is it over? A denied appeal is definitely not the end of the road. It’s simply a sign that you need to take a different approach. At this stage, your next steps could include filing a formal complaint with the Texas Department of Insurance or exploring legal action. This is the point where having an experienced property insurance attorney becomes essential to review your case and guide you on the most effective way to proceed.