Your commercial insurance policy is a complex legal contract, often filled with dense language and confusing exclusions designed to protect the insurer’s interests, not yours. When you file a claim, the insurance company will use this complexity to its advantage, interpreting clauses in a way that minimizes their payout. Suddenly, the protection you thought you had feels like an illusion. Understanding your rights and what your policy truly covers is the first step toward a fair outcome. This is where an experienced advocate makes all the difference. A dedicated McKinney commercial property claim lawyer can decipher your policy, challenge the insurer’s unfair interpretations, and build a powerful case to recover the full amount your business is rightfully owed.

Key Takeaways

- A lawyer manages the entire claims process for you: An experienced attorney acts as your professional advocate, handling everything from decoding complex policy language and documenting damages to negotiating with the insurance company on your behalf.

- Your claim’s strength depends on detailed evidence: Build a powerful case by thoroughly documenting all physical damage with photos, creating inventories of lost items, and gathering financial records to prove business interruption losses.

- Focus on proven expertise and trial readiness: When choosing a lawyer, prioritize their specific experience with Texas commercial claims, a successful track record, and credentials like Board Certification, as their willingness to go to trial provides critical leverage.

What Does a Commercial Property Claim Lawyer Do?

When your commercial property is damaged, the last thing you want is a lengthy battle with your insurance company. A commercial property claim lawyer steps in to manage the entire process for you, acting as your dedicated partner and advocate. Their job is to make sure your claim is handled fairly and that you receive the full compensation you’re entitled to under your policy. They take the weight off your shoulders so you can focus on running your business.

From the moment you hire them, a lawyer works to level the playing field. Insurance companies have teams of adjusters and attorneys working to protect their bottom line. Your lawyer’s sole focus is protecting yours. They handle all communications with the insurer, prepare and submit complex paperwork, and build a powerful case on your behalf. Whether they are negotiating a settlement or preparing for trial, their goal is to secure the resources you need to repair your property and recover your losses.

Acting as Your Advocate in Insurance Disputes

Think of a commercial property lawyer as your professional representative in any property insurance disputes. While some claims are simple, many become complicated, involving endless back-and-forth with the insurance adjuster or even an unfair denial. Your attorney manages all of these interactions, presenting your case clearly and firmly. They know the tactics insurers use to minimize payouts and are prepared to counter them with facts and legal arguments. This advocacy is crucial for negotiating a higher offer that accurately reflects the full extent of your damages, rather than settling for the first lowball number the insurance company provides.

Reviewing Your Policy and Documenting Damage

Commercial insurance policies are notoriously complex, filled with dense language and confusing exclusions. A key part of your lawyer’s job is to conduct a thorough policy review to identify every bit of coverage you are owed. At the same time, they help you gather and organize the critical evidence needed for a successful claim. Property damage documentation is essential. Your lawyer will help compile everything from photos and repair estimates to expert reports and financial records, ensuring your claim is supported by a strong foundation of proof. This is especially important when it comes to calculating and proving lost business income.

Negotiating and Litigating on Your Behalf

The primary goal is always to reach a fair settlement through negotiation. Your lawyer will present your documented claim to the insurance company and skillfully negotiate to get you the best possible outcome. However, if the insurer refuses to offer a fair settlement, a seasoned trial lawyer is ready to take your case to court. This willingness to litigate gives you significant leverage during negotiations. An attorney with a proven track record of successful results shows the insurance company you are serious about recovering what you are owed, even if it means fighting for it in front of a judge and jury.

What Are Common Commercial Property Claims in Texas?

As a business owner in Texas, you know that unexpected events can strike at any time. From severe weather to unforeseen accidents, damage to your commercial property can halt operations and create significant financial strain. Your insurance policy is supposed to be your safety net, but filing a claim is often just the first step in a challenging process. Understanding the most common types of claims can help you prepare for what’s ahead and recognize when you might need help. A Fort Worth property insurance lawyer can be a crucial ally when your insurer doesn’t hold up their end of the bargain. Let’s look at some of the frequent issues Texas business owners face.

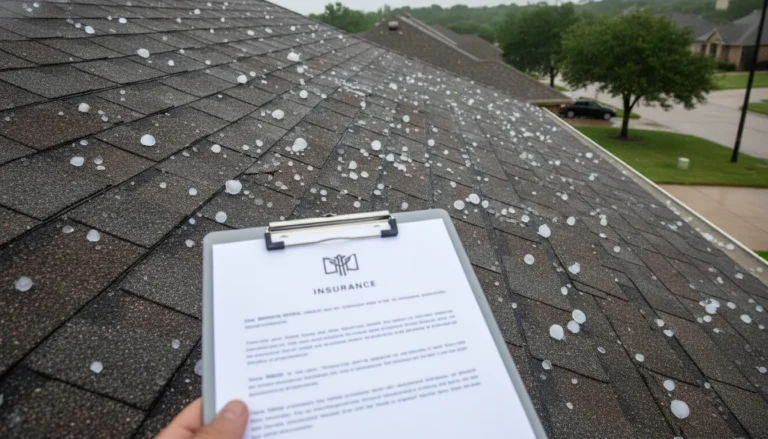

Storm, Hail, and Wind Damage

Texas weather is notoriously unpredictable. Severe storms, tornadoes, and hailstorms can cause widespread destruction in a matter of minutes. For commercial properties, this often means catastrophic damage to roofs, windows, siding, and even the structural integrity of the building. After a storm, you might be dealing with water intrusion that damages inventory and equipment inside. Insurance companies frequently challenge these claims by arguing the damage was pre-existing or by underestimating the cost of proper repairs. They might offer to pay for a simple patch job when a full roof replacement is what’s truly needed to protect your asset long-term.

Fire and Smoke Damage

A fire is one of the most devastating events a business can experience. The immediate destruction from the flames is obvious, but the damage rarely stops there. Smoke and soot can travel throughout your property, seeping into walls, ventilation systems, and inventory, causing damage far from the fire’s origin. The cleanup process is extensive and requires specialized techniques to eliminate odors and toxic residues. Unfortunately, insurers may try to downplay the severity of smoke damage or refuse to cover the full cost of restoration, leaving you with lingering problems that can affect the health of your employees and customers.

Water Damage and Flooding

Water damage is a frequent issue for commercial properties, and it doesn’t always come from a storm. A burst pipe from a sudden freeze, a failed plumbing fixture, or a leaky roof can lead to extensive damage very quickly. If not addressed immediately, this can result in ruined drywall, warped flooring, and dangerous mold growth. It’s important to know that standard commercial policies often distinguish between different types of water damage. For example, damage from a burst pipe is typically covered, while flooding from rising surface water usually requires a separate flood insurance policy, creating a common point of dispute with insurers.

Vandalism and Structural Failures

Your property can also be damaged by intentional acts or hidden structural problems. Vandalism, such as broken windows, graffiti, or theft, can leave you with significant repair costs and a sense of vulnerability. Separately, structural failures can occur due to construction defects, soil shifting, or design flaws, leading to issues like a collapsing wall or a failing foundation. In these cases, an insurer might try to deny the claim by blaming poor maintenance or arguing that the specific cause of the failure isn’t a covered event under your policy. Proving the cause and securing fair compensation often requires a thorough investigation, which is a key part of our firm’s practice areas.

Why Are Commercial Insurance Claims So Complicated?

When your business suffers damage, you expect your insurance policy to be the safety net you’ve paid for. Unfortunately, filing a commercial property claim is rarely straightforward. These claims are often complex because they involve detailed policies, significant financial stakes, and insurance companies motivated to protect their bottom line. For business owners in Texas, this process can feel like a full-time job, filled with confusing paperwork and frustrating negotiations. The insurer might request endless documentation, send adjusters who undervalue your damage, or simply stop responding to your calls. It’s a frustrating position to be in when you’re also trying to keep your business running. The reality is that the insurance company has a team of experts working to minimize their payout. They handle these claims every day and know how to use the fine print to their advantage. This puts you at an immediate disadvantage from the very beginning. The larger the claim, the more resistance you are likely to face, as the financial exposure for the insurer increases. Understanding the common hurdles they put in your way is the first step toward protecting your interests and getting the full compensation your business deserves.

Decoding Complex Policy Language

Commercial insurance policies are dense legal contracts, not simple agreements. They are filled with technical jargon, specific conditions, and lengthy exclusions that can be difficult to understand without a legal background. A single misinterpreted clause could lead an insurer to deny your claim. An experienced property insurance lawyer acts as your translator and advocate. They can analyze your policy to determine exactly what is covered, identify any potential loopholes the insurer might try to use, and ensure the insurance company is held to the terms of the contract you both agreed to.

Dealing with Lowball Settlement Offers

It’s a common tactic for an insurance company’s first settlement offer to be far less than what your claim is actually worth. Insurers may undervalue the cost of repairs, overlook certain types of damage, or fail to account for the full scope of your losses. Accepting a lowball offer can leave you paying out-of-pocket for repairs and other expenses. A skilled attorney can challenge an inadequate valuation by presenting detailed evidence of your damages and negotiating for a fair settlement that reflects the true cost of your recovery. Reviewing a firm’s past results can show you their experience in securing proper compensation for clients.

Overcoming Unfair Delays and Denials

Insurance companies are legally required to handle claims in a timely manner, but frustrating delays are all too common. Some insurers may drag out the process, hoping you’ll get discouraged and accept a lower payout. In other cases, they may deny a valid claim based on a minor technicality or an incorrect interpretation of your policy. These tactics can put an immense strain on your business operations. A lawyer can intervene by holding the insurer accountable to legal deadlines, formally challenging an unfair denial, and fighting back against any bad faith insurance practices.

Proving Business Interruption Losses

If property damage forces you to temporarily close your doors, business interruption coverage is designed to replace that lost income. However, proving these losses is a major challenge. It requires meticulous documentation, including past financial records, profit and loss statements, and realistic projections of what your business would have earned. Insurers scrutinize these claims carefully and often dispute the amount of lost income. An attorney can help you gather the necessary financial evidence and build a clear, compelling case to recover the income you lost while your business was out of commission.

How Can a Lawyer Help If Your Claim Is Denied or Underpaid?

It’s incredibly frustrating when the insurance company you’ve paid faithfully denies your claim or offers a settlement that doesn’t even begin to cover your losses. This is a critical moment, and you don’t have to accept their decision as final. An experienced commercial property claim lawyer can step in to challenge the insurer’s position and fight for the full amount you are owed. They become your advocate, handling the complex negotiations and legal hurdles so you can focus on your business. A lawyer systematically dismantles the insurer’s arguments by investigating their reasoning, building a more powerful case, and holding them accountable for unfair tactics.

Investigating the Insurer’s Reasoning

An insurer must explain why they denied or underpaid your claim, but their reasoning might be based on a confusing policy interpretation or a flawed damage assessment. An attorney’s first step is to investigate by demanding the complete claim file to understand their decision-making process. They will carefully analyze the adjuster’s notes, expert reports, and internal communications. An experienced property insurance lawyer compares this information against your policy to find inconsistencies or weak justifications for the denial. This detailed investigation often uncovers the leverage needed to reopen negotiations.

Building a Stronger Case with Evidence

While you may have submitted photos and estimates, an attorney builds a comprehensive case that is much harder for an insurer to dismiss. This involves gathering stronger evidence to counter the insurance company’s assessment. Your lawyer can bring in independent experts, like engineers, public adjusters, and contractors, to conduct their own thorough inspections. These experts provide detailed reports and credible testimony documenting the full extent of your property damage and financial losses. This powerful evidence strengthens your negotiating position and shows the insurer you are prepared to prove your damages at trial.

Fighting Bad Faith Insurance Tactics

Insurance companies have a legal duty to treat you fairly. When they use unreasonable delays, misrepresent your policy, or refuse to conduct a proper investigation, they may be acting in bad faith. These are pressure tactics designed to make you accept a lowball offer. A lawyer acts as your shield, protecting your rights as a policyholder and holding the insurer accountable. They know how to identify and document these bad faith practices. By formally challenging these actions, your attorney sends a clear message that you will not be intimidated and are prepared to take further legal action.

How Do You Choose the Right Commercial Property Lawyer?

Finding the right legal partner when your business is on the line can feel like a monumental task. You need someone who not only understands the law but also gets what’s at stake for you as a business owner. The key is to look for specific qualifications and qualities that separate a good lawyer from the right one for your case. By focusing on a few key areas like specialized expertise, relevant experience, and communication style, you can confidently choose an advocate who is equipped to handle the complexities of your commercial property claim and fight for the compensation you deserve.

Look for Board Certification and Trial Experience

When you’re vetting lawyers, one of the most important credentials to look for is Board Certification. Think of it as an expert-level qualification. In Texas, a lawyer who is Board Certified in a specialty like Personal Injury Trial Law has passed a rigorous exam and demonstrated extensive experience in that field. This certification is a clear sign that they have a deep understanding of the legal landscape. You also want a lawyer with significant trial experience. Many cases settle out of court, but you need an attorney who isn’t afraid to take your case to trial if the insurance company refuses to offer a fair settlement. Their readiness to go to court often gives you more leverage during negotiations.

Verify Their Track Record with Commercial Claims

Not all property damage claims are the same. A lawyer who primarily handles residential claims may not have the specific experience needed for your case. Commercial claims are far more complex, often involving issues like business interruption, lost income, and damage to specialized equipment. Ask any potential attorney about their specific history with commercial claims. Look for a proven track record of successfully representing businesses like yours. They should be able to point to past cases that show they know how to value your losses accurately and build a strong case on your behalf. A lawyer with direct experience in this area will be better prepared for the unique challenges your business faces.

Confirm Their Knowledge of Texas Insurance Law

Insurance law varies significantly from state to state, so hiring a lawyer with a deep understanding of Texas regulations is non-negotiable. Your attorney needs to be an expert on the Texas Insurance Code, including the laws that protect policyholders from bad faith practices. A Fort Worth property insurance lawyer will be familiar with local court procedures and have experience dealing with the specific insurance companies that operate in our state. This local knowledge can be a major advantage, ensuring your claim is handled correctly and that your rights as a Texas policyholder are protected every step of the way. They will know the tactics insurers use and how to counter them effectively under state law.

Check Client Reviews and Communication Style

Legal expertise is critical, but so is finding a lawyer you can trust and communicate with effectively. Before making a decision, take the time to read client testimonials and reviews. See what past clients have to say about the lawyer’s responsiveness, clarity, and overall approach. During your initial consultation, pay attention to how they communicate. Do they listen to your concerns? Do they explain complex legal concepts in a way you can understand? You’ll be working closely with this person during a stressful time, so it’s important to find an advocate who is not only a skilled attorney but also a supportive and clear communicator.

How Do Property Claim Lawyers Get Paid?

When your business is facing significant losses from property damage, the last thing you want to worry about is how to afford legal help. Fortunately, most reputable property claim lawyers in Texas work on a contingency fee basis. This payment structure is designed to give you access to high-quality legal representation without any upfront financial risk, allowing you to focus on getting your business back on its feet. It aligns your lawyer’s goals with yours: getting you the best possible recovery from the insurance company.

Understanding Contingency Fee Agreements

A contingency fee agreement means your lawyer’s payment is contingent on the outcome of your case. You don’t pay any attorney’s fees out of pocket. Instead, the lawyer receives a pre-agreed-upon percentage of the financial settlement or verdict they secure for you. This model ensures that everyone, from small business owners to large commercial enterprises, can stand up to their insurance carrier.

Typically, this percentage is around one-third of the recovery if the case settles before a lawsuit is filed. If the case proceeds to litigation, the fee might increase to around 40% to account for the additional time and resources required. This structure is a core part of many legal practice areas focused on helping policyholders.

What “No Recovery, No Fee” Means for You

The phrase “no recovery, no fee” is the cornerstone of a contingency agreement. It’s a straightforward promise: if your attorney doesn’t win your case, you don’t owe them any legal fees for their time and effort. This arrangement effectively removes the financial risk from your shoulders. You can pursue the compensation you deserve without the fear of ending up with a large legal bill if the case is unsuccessful.

This model also demonstrates an attorney’s confidence in your claim. A lawyer working on contingency will carefully evaluate your case from the start because they only get paid if they deliver positive results. It’s a powerful way to ensure your legal team is fully invested in achieving a successful outcome for your business.

The Importance of Transparent Legal Costs

While the contingency fee covers your attorney’s services, every legal case involves other expenses. These can include court filing fees, costs for hiring expert witnesses like engineers or public adjusters, and expenses for depositions. A trustworthy lawyer will be completely transparent about these potential costs from your very first meeting.

Your fee agreement should clearly outline how these expenses are handled. Will they be deducted from your settlement? If so, are they taken out before or after the attorney’s percentage is calculated? A dedicated attorney like Tim Hoch will walk you through every detail of the agreement, ensuring you understand all aspects of the financial arrangement. This transparency is key to building a strong, trusting relationship with your legal team.

How to Prepare for Your First Legal Consultation

Walking into a lawyer’s office can feel overwhelming, especially when you’re already managing the stress of significant property damage. A little preparation, however, can make a world of difference. When you arrive at your first consultation with your information organized, you help your potential attorney get a clear picture of your situation right away. This allows them to offer more specific advice and outline a solid plan for what comes next. Think of it as giving your legal team a head start on building your case.

A productive first meeting sets the tone for your entire claim. It helps you determine if the lawyer is the right fit and allows them to assess the strengths of your case from the very beginning. By taking a few key steps to get your documents in order, you can walk in feeling confident and ready to have a meaningful conversation. Here’s a straightforward guide on what you can do to get ready for your meeting and ensure you cover all the essential practice areas related to your claim.

Gather Your Key Insurance Documents

The most important document in your case is your commercial property insurance policy. I’m not talking about the summary or declarations page, but the entire policy packet. This document outlines exactly what your insurer is obligated to cover and what your responsibilities are as the policyholder. If you can’t find your complete copy, you should immediately request a full, certified version from your insurance company. Having the full policy allows a Fort Worth property insurance lawyer to analyze the specific language, identify all applicable coverages, and spot any tricky exclusions the insurer might try to use against you. Bring this document, along with any endorsements or addendums, to your consultation.

Organize Your Photos and Damage Evidence

A picture is worth a thousand words, and in an insurance claim, it can be worth thousands of dollars. Before any cleanup or repairs begin, you need to thoroughly document the damage to your property. Take more photos and videos than you think you need from every possible angle. Be sure to get wide shots of the affected areas as well as close-ups of specific damage points. The more evidence you have, the better. Keep your files organized, perhaps in a digital folder labeled with the date the damage occurred. This visual proof is your strongest tool for showing the true extent of your losses and countering an insurer’s attempts to downplay the severity of the situation.

Collect All Correspondence with Your Insurer

Every single interaction you have with your insurance company matters. Start a dedicated file, physical or digital, and keep a complete record of all communications. This includes every email, letter, and text message exchanged with the adjuster or other company representatives. For phone calls, it’s wise to keep a simple log noting the date, time, the person you spoke with, and a brief summary of what was discussed. This detailed timeline can be incredibly valuable, as it can reveal patterns of delay, contradictory statements, or other unfair tactics. Providing your attorney with this organized record gives them immediate insight into how the insurer has handled your claim so far.

What Documentation Do You Need for a Strong Claim?

When your business property is damaged, it feels like everything is on hold. The path back to normal operations runs directly through your insurance claim, and the strength of that claim depends entirely on your documentation. Think of it as building a case for your business’s recovery. The more organized and thorough your evidence is, the harder it is for an insurance company to justify a delay, a lowball offer, or an outright denial. A well-documented claim shows the insurer you are serious and prepared to prove the full extent of your losses, leaving little room for dispute.

This isn’t just about having a few photos on your phone. It’s about creating a comprehensive file that tells the complete story of your damages and financial impact. From detailed inventories and financial records to expert reports, each piece of paper adds weight to your position. While it can feel like a lot to manage, especially when you’re trying to keep your business afloat, this step is crucial for a fair outcome. A Fort Worth property insurance lawyer can guide you through this process, ensuring you collect the right information to build an undeniable claim and fight for the full compensation you deserve.

Evidence of Property Damage

Your first priority should be documenting the physical damage to your property. Solid evidence is essential for any business property claim. Start by taking extensive photos and videos from every possible angle, capturing both wide shots of the affected areas and close-ups of specific damage. If you have “before” photos, include them for comparison. Next, create a detailed inventory of every damaged item, from office equipment and machinery to furniture and stock. For each item, note its description, age, purchase price, and estimated replacement cost. Finally, gather any receipts, invoices, or repair estimates from contractors. This collection of evidence forms the foundation of your claim.

Proof of Financial Losses

Damage to your building is only part of the story. Many commercial policies cover business interruption, which compensates you for income lost while your business is closed or operating at a reduced capacity. To prove these losses, you’ll need to pull together key financial documents. Gather your profit and loss statements, sales records, bank statements, and tax returns from before and after the incident. These records help establish a baseline for your typical revenue. An experienced attorney can help you gather the right evidence and negotiate a fair settlement for your lost business income, ensuring your financial recovery is as complete as your physical one.

Reports from Professional Assessors

Sometimes, the insurance company’s adjuster may overlook or undervalue certain aspects of your damage. This is where independent experts come in. Hiring a public adjuster, structural engineer, or specialized contractor to assess the damage can provide a credible, third-party evaluation of your losses. Their detailed reports can challenge the insurer’s findings and provide powerful leverage during negotiations. Business owners often find it tough to manage the complexities of commercial property damage claims on their own. A lawyer with deep experience in these matters, like Board Certified trial lawyer Tim Hoch, can connect you with trusted professionals and use their findings to build a more compelling case.

Related Articles

- Commercial Property Insurance Claims Attorney | Hoch Law Firm, PC

- Property Insurance Claims Process in Dallas | Hoch Law Firm, PC

- Property Insurance Claim? How Long Do You Have to Sue? – Hoch Law Firm, PC

- Property Insurance Claim? You May Be In for a Surprise – Hoch Law Firm, PC

Frequently Asked Questions

When is the best time to contact a commercial property lawyer? The ideal time to contact a lawyer is as soon as you discover significant damage, even before you file the claim. An attorney can help you document the damage correctly from the start and manage all communications with the insurer, which prevents you from making any missteps that could harm your claim later. However, it is never too late to seek legal advice, especially if you are facing delays, a low settlement offer, or an outright denial.

My insurance adjuster seems friendly and helpful. Why would I need an attorney? It’s important to remember that even the most personable insurance adjuster works for the insurance company, not for you. Their primary responsibility is to protect their employer’s financial interests, which often means minimizing the amount paid out on claims. An attorney, on the other hand, is your exclusive advocate. Their only job is to protect your interests and fight to get you the full and fair compensation you are entitled to under your policy.

What if my claim has already been denied? Is it too late to hire a lawyer? Absolutely not. A claim denial is often the point when hiring an attorney becomes most critical. A lawyer can thoroughly investigate the insurance company’s reason for the denial, review your policy to challenge their interpretation, and build a much stronger case with new evidence and expert opinions. A denial is not the end of the road; it’s simply the start of a new phase in fighting for your claim.

Can a lawyer help me prove my lost business income? Yes, this is a key area where an attorney provides significant value. Proving business interruption losses is complicated because it requires detailed financial documentation and projections. A lawyer knows exactly what evidence is needed, such as past profit and loss statements and sales records, and can help you present it in a clear, compelling way. They work to ensure your claim accounts for the full financial impact the property damage has had on your operations.

You mention Board Certification. What does that actually mean for my case? Board Certification is a mark of true expertise in a specific area of law. For a lawyer to become Board Certified in Texas, they must have extensive trial experience, pass a difficult specialty exam, and be favorably evaluated by their peers. Choosing a Board Certified lawyer means you are hiring someone with a proven, high-level understanding of trial law. This level of expertise gives you a significant advantage when negotiating with an insurance company or, if necessary, presenting your case in court.