Your insurance policy is a contract. You held up your end by paying your premiums; now, your insurer must hold up theirs. When a storm damages your property, you are not asking for a handout—you are demanding what you are rightfully owed. Unfortunately, insurance companies can make you feel like you’re fighting an uphill battle alone. They may try to undervalue your losses or deny your claim based on a technicality. Don’t let them dictate the value of your property. You can take control of the situation. By documenting everything, understanding your policy, and knowing when to bring in a professional, you can build a powerful case. A tenacious wind damage insurance lawyer Arlington can be the key to holding your insurer accountable. Let’s explore the steps you can take to secure the fair payment you deserve.

Key Takeaways

- Build your case from day one: Your most powerful evidence is created right after the storm. Thoroughly document all damage with photos, make temporary repairs to prevent further issues, and keep a detailed log of every communication.

- Challenge low offers and confusing denials: Insurance companies often try to underpay claims by blaming pre-existing damage or using complex policy language. You have the right to question their assessment and fight for a fair amount.

- Professional help is more accessible than you think: A property insurance lawyer can handle the entire claims process for you. They level the playing field with the insurer and typically work on a contingency fee, so you pay no upfront costs.

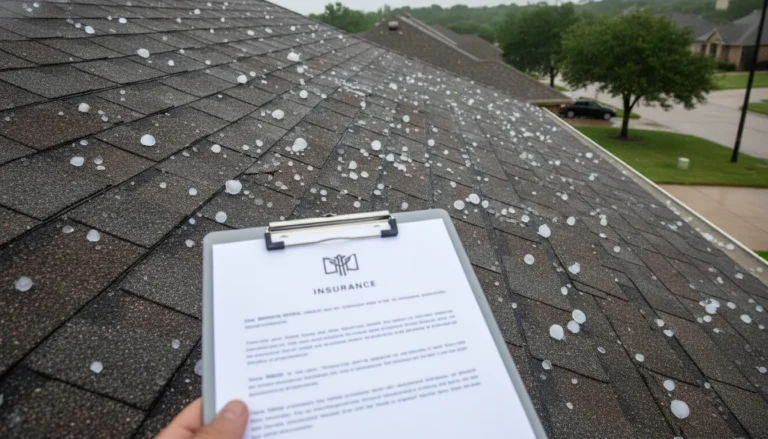

Your First Steps After Wind Damage in Arlington

When a severe storm hits Arlington, the aftermath can feel chaotic. But the steps you take immediately following the wind damage are critical for the success of your insurance claim. Acting quickly and methodically can make all the difference between a smooth process and a frustrating battle with your insurer. Think of this as building your case from day one. By carefully documenting everything and communicating clearly, you protect your rights and set the stage for receiving the fair compensation you need to repair your property.

Document All the Damage

Your smartphone is your best tool right after a storm. Before you move anything or start cleaning up, take extensive photos and videos of all the damage. Capture everything from multiple angles, getting both wide shots to show the overall scene and close-ups of specific issues like dented siding, missing shingles, or broken windows. Don’t forget to document any interior damage caused by water leaks. This visual evidence is your most powerful proof of loss. Keep a detailed inventory of all damaged personal belongings as well. This documentation will be essential when you file your claim and can help counter any attempts by the insurance company to downplay the extent of your losses.

Make Temporary Repairs to Prevent More Damage

Your insurance policy likely requires you to take reasonable steps to prevent further damage to your property after a storm. This is often called your “duty to mitigate damages.” This doesn’t mean starting permanent repairs; it means making temporary fixes to secure your home or business. For example, you might place a tarp over a hole in your roof to stop leaks or board up a shattered window to keep the elements out. Be sure to save every receipt for materials you buy for these temporary repairs, like tarps, plywood, or plastic sheeting. These costs should be a reimbursable part of your property insurance claim.

Contact Your Insurance Company Right Away

Notify your insurance provider about the damage as soon as it is safe to do so. Most policies have rules about how quickly you must report a claim. When you call, stick to the facts you know. Provide your policy number, describe the event (e.g., “high winds from the storm on Tuesday night”), and give a general overview of the damage you can see. Avoid speculating on the full extent of the damage or accepting blame. This initial call officially starts the claims process and gets an adjuster assigned to your case. Having a clear record of this first contact is an important part of managing your claim from the beginning.

Get Several Professional Repair Estimates

Don’t rely solely on the estimate from the insurance adjuster. To understand the true cost of repairs, get written estimates from at least two or three reputable, local contractors. These professionals can often spot hidden damage that an adjuster might miss. Providing multiple estimates to your insurer demonstrates that you’ve done your homework and strengthens your position during negotiations. These detailed quotes serve as powerful evidence to support your claim for the full amount needed to restore your property. Make sure each estimate is itemized, breaking down the costs for labor and materials, so you can clearly justify your requested settlement amount.

Keep a Detailed Log of All Communications

From your very first call to your insurance company, keep a meticulous record of every interaction. Get a dedicated notebook or start a digital document to log all communications. For every phone call, email, or letter, write down the date, time, the name of the person you spoke with, and a summary of what was discussed. If you send an email, save it. If you have a phone call, follow up with a brief email confirming what was said. This communication log creates a timeline of your claim and can be invaluable if a dispute arises. It helps you stay organized and provides a factual record to hold your insurer accountable.

Why Wind Damage Claims Get Denied or Underpaid

After the stress of a major storm, the last thing you want is a fight with your insurance company. Unfortunately, getting a fair settlement for wind damage isn’t always straightforward. Insurers may deny or underpay valid claims for several reasons, leaving you to cover the costs of repairs yourself. Understanding these common hurdles is the first step toward protecting your rights and getting the compensation you deserve.

Confusing Policy Language and Exclusions

Insurance policies are dense legal contracts filled with complex language, specific definitions, and pages of exclusions. It’s easy to feel lost in the fine print. An insurer might point to a specific clause you’ve never heard of to justify denying your claim. For example, they may argue that the damage was caused by a combination of wind and rain (or flooding), and their policy only covers one or the other. Because insurance companies are businesses, they often use this complexity to their advantage, hoping you won’t question their interpretation. A Fort Worth property insurance lawyer can help you understand exactly what your policy covers and hold your insurer to their promises.

Not Enough Proof of Your Loss

The responsibility to prove your losses falls on you, the policyholder. If your documentation is weak, the insurance company has an easy reason to push back. They might claim there isn’t enough detailed proof connecting the storm to the damage on your property. This is why it’s so important to take clear photos and videos of the damage from every angle immediately after the storm. You should also keep detailed records of every conversation, email, and expense related to your claim. Without strong evidence, the insurer can argue that the damage isn’t as severe as you claim or that it wasn’t caused by the covered event, leaving you with an unfairly low settlement or an outright denial.

Arguments Over Pre-Existing Damage

One of the most common tactics used by insurance adjusters is to blame the damage on pre-existing issues. They will inspect your property looking for signs of wear and tear, poor maintenance, or old, unrepaired problems. They might then argue that the wind didn’t cause the damage but simply worsened an existing condition that isn’t covered by your policy. For example, they could claim your roof was already old and failing before the storm hit. This allows them to drastically reduce your settlement or deny the claim entirely. Contesting these arguments requires a clear understanding of your policy and strong evidence showing the storm was the direct cause of the damage.

Bad Faith Tactics from the Insurance Company

Sometimes, a denial or low offer isn’t just a disagreement; it’s a sign of bad faith. Insurance companies have a legal duty to treat you fairly and handle your claim honestly. When they fail to do so, it’s known as acting in bad faith. This can include unreasonably delaying the claims process, refusing to conduct a thorough investigation, misrepresenting what your policy covers, or making a settlement offer that is far below what your claim is worth. These tactics are designed to wear you down and pressure you into accepting less than you’re owed. Recognizing these actions is key to fighting back against unfair treatment from your insurer.

How a Wind Damage Lawyer Can Help You

When you’re dealing with the aftermath of a storm, the last thing you want is a battle with your insurance company. A wind damage lawyer steps in to manage the entire claims process for you, making sure your rights are protected from start to finish. They handle the complicated paperwork, the tough negotiations, and the legal strategy, so you can focus on getting your property and life back in order. Think of them as your professional advocate, dedicated to securing the fair outcome you deserve.

Hiring an attorney isn’t just for when things go wrong; it’s a proactive step to prevent them from going wrong in the first place. From the moment you bring them on, they take over communication with the insurer, which immediately signals that you are serious about your claim. This can prevent the lowball offers and unnecessary delays that policyholders often face when they handle claims alone. Your lawyer will create a comprehensive strategy tailored to your specific situation, anticipating the insurance company’s arguments and preparing strong counter-arguments backed by solid evidence. They work to resolve your claim efficiently and fairly through negotiation, but they are always prepared to take stronger action if needed. With an expert on your side, you can feel confident that every detail is being handled correctly and that you’re taking the right steps to recover your losses without the added stress of fighting an insurance giant by yourself.

Review Your Insurance Policy

Insurance policies can feel like they’re written in another language, filled with confusing clauses and technical jargon. An experienced attorney can translate it all for you. They will conduct a thorough review of your policy to determine exactly what’s covered and identify any potential loopholes the insurance company might try to use against you. Understanding the fine print is the first step to building a strong claim. A lawyer ensures you know your rights and what you’re entitled to, setting a solid foundation for the entire property insurance claims process and preventing the insurer from misinterpreting your coverage.

Gather Key Evidence for Your Claim

A successful wind damage claim depends on solid proof. A lawyer knows exactly what evidence is needed to build an undeniable case for the insurance company. They will guide you in documenting everything, from taking detailed photos and videos of the damage to obtaining multiple, credible repair estimates from trusted contractors. They can also bring in engineers or public adjusters to create expert reports that validate the extent of your loss. This comprehensive collection of evidence leaves little room for the insurer to dispute the facts, strengthening your position and making it much harder for them to underpay or deny your claim.

Negotiate with Your Insurer

Going up against an insurance adjuster can be intimidating. They are trained negotiators whose goal is often to settle for the lowest amount possible. Having a lawyer on your side levels the playing field. Your attorney will handle all communications with the insurance company, presenting your evidence and arguing on your behalf. They know the tactics insurers use and how to counter them effectively. If you receive a lowball offer, your lawyer will fight back, negotiating for the full and fair settlement you need to make proper repairs. Their experience in these negotiations can make a significant difference in the final results of your claim.

Represent You in Court if Necessary

Sometimes, an insurance company simply refuses to be fair, no matter how strong your evidence is. If negotiations stall, your lawyer’s ability to file a lawsuit is your most powerful tool. This step is something only an attorney can take. The mere threat of litigation often persuades an insurer to offer a better settlement. If they still won’t budge, a Board Certified trial lawyer is prepared to take your case to court. They will fight to hold the insurance company accountable for their obligations and can even pursue additional damages if the insurer acted in bad faith.

Signs You Need to Call a Wind Damage Lawyer

After a storm, you expect your insurance company to help you put the pieces back together. You’ve paid your premiums, and now it’s their turn to hold up their end of the bargain. But what happens when they don’t? The claims process can quickly become confusing and adversarial, leaving you to wonder if you’re being treated fairly.

While many claims go smoothly, certain red flags signal that it’s time to get professional legal help. An experienced attorney can step in to protect your rights and make sure your insurer honors its obligations. If you find yourself in any of the following situations, it’s a good idea to consult with a lawyer who handles property insurance disputes and can guide you on the best path forward.

Your Claim Is Unfairly Delayed or Denied

Insurance companies in Texas are required to handle claims in a timely manner. If your adjuster is unresponsive, weeks turn into months without a decision, or the company keeps asking for the same documents over and over, they may be engaging in delay tactics. An outright denial with a vague or confusing explanation is an even bigger warning sign. You shouldn’t have to fight for basic communication or a clear answer. A lawyer can step in to demand action and hold the insurer accountable for these delays or an unjust denial.

You Get a Lowball Settlement Offer

The first settlement offer from an insurance company is rarely its best. Insurers are businesses, and their goal is often to pay out as little as possible. If you receive an offer that doesn’t even come close to covering your contractors’ repair estimates, don’t feel pressured to accept it. This is a classic sign that your insurer is undervaluing your claim. An attorney with a proven record of success can assess the true value of your damages and negotiate for the full and fair compensation you need to make proper repairs.

The Insurer Says Your Damage Isn’t Covered

Insurance policies are notoriously complex. An adjuster might tell you the specific type of wind damage to your roof isn’t covered, that the damage was pre-existing, or that you’ve missed a detail in the fine print. These arguments can be difficult to counter on your own. An experienced lawyer knows how to interpret your policy correctly, challenge unfair coverage denials, and find the language that supports your claim. Don’t just take the insurance company’s word for it; get a professional opinion.

You Feel Overwhelmed by the Claims Process

Recovering from storm damage is stressful enough. You shouldn’t also have to become an expert in insurance law, construction, and negotiation overnight. If you feel overwhelmed by the paperwork, intimidated by the adjuster, or simply unsure of what to do next, that’s a perfectly good reason to ask for help. Bringing in an experienced advocate to manage the process allows you to focus on your family or business. A lawyer can handle the communications, paperwork, and negotiations, giving you peace of mind that your claim is in capable hands.

Fighting a Denied or Underpaid Claim? Here’s How a Lawyer Helps

Receiving a denial letter or a shockingly low settlement offer from your insurance company can feel like a final blow. But it doesn’t have to be the end of the road. An experienced property insurance lawyer can step in to champion your case, turning a frustrating situation into a fair resolution. They have the skills and legal knowledge to hold your insurer accountable and fight for the full compensation you deserve. Here’s exactly how they can make a difference.

Challenge Unfair Claim Denials

Many homeowners and businesses in Texas face the stress of a denied wind damage claim. When your insurer says “no,” it’s easy to feel defeated, but their decision is not the final word. An attorney can systematically challenge an unfair denial by re-examining your policy, the adjuster’s report, and all the evidence. They know what it takes to build a compelling case that demonstrates why your claim is valid. By presenting new evidence or highlighting errors in the insurer’s assessment, a lawyer can often get a denial overturned, putting you back on the path to recovery.

Fight Undervalued Settlements

Insurance companies often make lowball settlement offers, hoping you’ll accept a quick payout without questioning it. These offers rarely cover the full cost of repairs, leaving you to pay the difference out of pocket. You can and should challenge their decision with strong evidence. A skilled lawyer will bring in their own network of trusted contractors and public adjusters to create an independent and accurate estimate of your damages. Armed with this detailed assessment, they can negotiate aggressively with the insurance company to secure a settlement that truly reflects the cost of restoring your property.

Find Overlooked Coverage in Your Policy

Insurance policies are notoriously complex, filled with dense language and confusing exclusions. It’s easy to miss important details. A lawyer can level the playing field because they understand insurance law and know how to interpret these documents. They can conduct a thorough review of your policy to find sources of coverage you might have overlooked. Sometimes, a provision buried in the fine print can make all the difference. This expert analysis ensures you are using every part of your policy to your advantage and fighting back against any attempts by the insurer to misrepresent your coverage.

Handle Insurance Company Bad Faith

When you pay your premiums, you trust your insurer to act in good faith. Unfortunately, that doesn’t always happen. Insurance companies sometimes deny valid claims, cause unreasonable delays, or fail to investigate properly. These actions may constitute “bad faith.” An attorney can identify these tactics and hold the insurer accountable for not upholding their legal obligations. Proving bad faith can not only get your original claim paid but may also entitle you to additional damages. Having a lawyer who has a proven record of success sends a clear message that you won’t be taken advantage of.

What to Look for in an Arlington Wind Damage Lawyer

Choosing the right lawyer can feel like a monumental task, especially when you’re already dealing with the stress of property damage. You need an advocate who not only understands the law but also gets what you’re going through. The right attorney will be your partner, guiding you through the complexities of the insurance claims process and fighting for the fair outcome you deserve. When you start your search, focus on a few key qualities that separate a good lawyer from a great one. Look for deep local experience, verified credentials, a history of winning cases like yours, and a genuine commitment to their clients.

Deep Experience in Texas Property Claims

Texas has its own unique weather patterns and a specific set of insurance laws. You want a lawyer who is deeply familiar with this landscape. Look for a firm that focuses on helping Texas property owners with their insurance claims, particularly cases that have been unfairly denied, delayed, or underpaid. An attorney with a strong background in Fort Worth property insurance disputes will understand the tactics local insurance adjusters use and know how to build a case that stands up to their scrutiny. This local expertise is invaluable and can make a significant difference in the outcome of your claim.

Board Certification and Strong Credentials

Not all lawyers have the same level of expertise. Board Certification is a mark of distinction that shows an attorney has gone above and beyond to prove their knowledge and skill in a specific area of law. For example, Tim Hoch is Board Certified in Personal Injury Trial Law by the Texas Board of Legal Specialization, an achievement earned by only a small percentage of Texas attorneys. This kind of credential demonstrates a serious commitment to their practice. When you’re vetting potential lawyers, always ask about their qualifications and look for proof of specialized training and recognition in property or trial law.

A Proven Record of Success

Experience is important, but a history of positive outcomes is what truly matters. You need a lawyer who not only talks the talk but has a demonstrated track record of securing fair settlements and verdicts for their clients. Don’t be shy about asking for case results or testimonials. A confident and successful law firm will be transparent about its past performance. Seeing a history of substantial results for clients gives you confidence that your case is in capable hands and that the firm has the resources and determination to fight for you all the way to the finish line.

Clear Communication and a Client-First Approach

The legal process can be confusing, and the last thing you need is a lawyer who speaks in complicated jargon. A great attorney will take the time to explain your policy, outline your options, and keep you informed every step of the way. They should be your trusted advisor, helping you understand your rights and making you feel supported. This client-first approach means they listen to your concerns, answer your questions promptly, and always act in your best interest. Their goal should be to lift the burden off your shoulders so you can focus on rebuilding.

What Does It Cost to Hire a Wind Damage Lawyer?

After a storm damages your property, the last thing you need is another bill. Many people hesitate to call a lawyer because they’re worried about the cost. But getting professional legal help for your insurance claim is more accessible than you might think. Understanding how attorney fees work can give you the confidence to get the support you need to fight for a fair settlement.

How Contingency Fee Agreements Work

Most property damage attorneys in Texas handle cases on a contingent fee basis. This is a straightforward arrangement: you don’t pay any attorney’s fees unless and until your lawyer wins your case. The firm’s payment is a pre-agreed-upon percentage of the financial recovery they secure for you, whether through a settlement or a court verdict. This approach aligns our goals with yours. We are invested in getting you the best possible outcome because we only succeed when you do. It’s a partnership focused on making sure the insurance company pays what you are rightfully owed for your property insurance dispute.

You Pay No Upfront Fees

With a contingency fee agreement, you don’t have to pay any money upfront to hire a wind damage lawyer. All the initial costs of building your case, from filing fees to hiring experts, are covered by the law firm. This removes the financial barrier that prevents many property owners from seeking justice. You can get an experienced legal advocate on your side right away without adding to your financial stress. This allows you to focus on repairing your property and getting your life back on track while your attorney handles the fight with the insurance company. Our firm’s proven results show our commitment to helping clients without adding to their financial burden.

Why Professional Help Is a Smart Investment

Hiring an attorney isn’t just another expense; it’s an investment in your claim’s success. Getting a lawyer involved early shows the insurer you are serious and helps you avoid critical mistakes that could weaken your case. Insurance companies have teams of adjusters and lawyers working to protect their bottom line. An experienced attorney levels the playing field. They can identify undervalued estimates, find coverage you may have missed, and negotiate for a much higher settlement than you might get on your own. Often, the increase in the final payout far exceeds the attorney’s fee, making legal representation a smart financial decision.

Related Articles

- Why Hire an Arlington Wind Damage Claim Attorney?

- Dallas Wind & Storm Damage Lawyer | Hoch Law Firm

- 5 Signs You Need to Hire an Attorney for Wind Damage

- Storm Damage Claims – Hoch Law Firm, PC

- Why Hire a Commercial Storm Damage Lawyer in Fort Worth?

Frequently Asked Questions

What if my insurance company’s offer seems low, but I’m not sure if it’s unfair? Trust your gut. If the settlement offer doesn’t feel right or won’t cover the repair estimates you’ve received from local contractors, it’s worth investigating. An insurer’s first offer is often just a starting point for negotiations. A good next step is to compare their itemized estimate against the ones from your chosen professionals. If there are major differences, an experienced attorney can review all the documents to determine the true value of your claim and help you build a case for the full amount you need.

Do I have to use the contractor my insurance company recommends? No, you are not required to use your insurer’s preferred contractor. In Texas, you have the right to choose a reputable, licensed contractor that you trust to repair your property. While the insurance company’s recommendation might seem convenient, it’s always wise to get several independent estimates. This ensures the scope of work is accurate and the pricing is fair, giving you control over the quality of the repairs to your home or business.

I already accepted and cashed a check from my insurer. Is it too late to get more money for my claim? Not necessarily. Cashing a check from the insurance company doesn’t always mean your claim is closed forever. If you discover additional damage later on or realize the initial payment was not enough to cover all the repairs, you may still be able to reopen the claim and negotiate for a supplemental payment. It’s a complex situation, so this is an ideal time to consult with a lawyer who can review the specifics of your case and advise you on the best path forward.

How soon after the damage occurs should I think about contacting a lawyer? You can contact a lawyer at any point in the claims process, but getting help early can prevent many common problems. If you anticipate a complicated claim, feel overwhelmed by the process, or simply want to ensure everything is handled correctly from day one, an initial consultation can be very helpful. It’s especially important to call if you experience any red flags, like significant delays, a lowball offer, or a confusing denial letter from your insurer.

What is the main difference between what a public adjuster does and what a lawyer does? A public adjuster is great at assessing and documenting the extent of your property damage to help you file a claim. However, their role ends there. A lawyer can do everything a public adjuster does and more. They can provide legal advice, interpret your policy, negotiate with the insurer, and, most importantly, file a lawsuit if the insurance company acts in bad faith or refuses to offer a fair settlement. Only a lawyer can take your case to court to hold the insurer legally accountable.