It’s a tough pill to swallow, but insurance companies are for-profit businesses. Their primary goal is to generate revenue, which often means paying out as little as possible on claims. While you see your policy as a safety net, they may see your claim as a line item on a balance sheet. This is why they use confusing policy language, strict deadlines, and lowball offers to protect their profits. When your valid claim is denied or underpaid, it feels personal, but it’s often just their business strategy. A commercial insurance claim dispute attorney understands this dynamic perfectly. They are experts at dismantling these strategies and forcing insurers to honor their contractual obligations. Here, we’ll explore the common reasons claims are denied and how an attorney fights back.

Key Takeaways

- Hire a specialist for a specialized problem: A general business lawyer is great for contracts, but an insurance dispute requires an attorney who lives and breathes insurance law. They know the specific tactics insurers use and focus solely on fighting for policyholders.

- Prioritize trial experience and board certification: These credentials are not just for show; they are your leverage. Insurance companies know which lawyers are willing to go to court, and that readiness often leads to much better settlement offers.

- Treat a denial letter as your call to action: A denial is not the final word. It’s your cue to stop talking to the insurer, gather all your documents, and immediately contact an experienced attorney to take over the fight for you.

What a Commercial Insurance Claim Dispute Attorney Does

When you run a business, you buy commercial insurance for peace of mind. You trust that if a disaster like a fire, hailstorm, or major theft occurs, your insurer will be there to help you recover. But what happens when the company you’ve paid faithfully denies your claim or offers a settlement that barely covers a fraction of your losses? That’s when a commercial insurance claim dispute attorney becomes your most important advocate.

This type of lawyer specializes in one thing: representing policyholders in disagreements with their insurance companies. They are experts in the complex world of insurance law and work exclusively for businesses and individuals, not the big carriers. Their entire focus is on making sure the insurer honors the policy you paid for. From deciphering confusing policy language to documenting your losses and fighting back against a wrongful denial, their job is to level the playing field and secure the full compensation your business needs to get back on its feet. They handle a wide range of practice areas, including property damage, business interruption, and bad faith claims.

How Are They Different From a General Business Attorney?

You might already have a great relationship with a general business attorney who helps with contracts or corporate filings, but handling an insurance dispute is a different ballgame. While a general business lawyer has a broad knowledge of commercial law, an insurance dispute attorney has a deep, specialized focus. They live and breathe insurance policies, state regulations, and the tactics insurers use to minimize payouts.

Think of it like seeing a specialist for a specific health issue. Your family doctor is fantastic for general wellness, but you’d want a cardiologist for a heart problem. An insurance dispute attorney is that specialist for your claim. They understand the nuances of proving your case and won’t be caught off guard by obscure policy exclusions or procedural tricks.

Why Board Certification and Trial Experience Are Crucial

When you’re looking for an attorney, you’ll see a lot of different credentials, but two that truly matter in this field are board certification and trial experience. An attorney who is Board Certified in Personal Injury Trial Law, for example, has been recognized by the Texas Board of Legal Specialization as an expert in their field. This isn’t an award they can buy; it requires extensive trial experience, peer reviews, and passing a rigorous exam.

This trial-ready status gives you incredible leverage. Insurance companies are businesses, and they make calculated decisions. They know which law firms are willing to go to court and which ones prefer to settle quickly for less. Hiring an attorney with proven trial experience and credentials sends a clear message: you are prepared to fight for what you’re owed, all the way to a jury verdict if necessary.

What Kinds of Disputes Do They Handle?

A commercial insurance dispute attorney is your advocate when your insurance company fails to meet its obligations. Their work isn’t just about one type of claim; it covers a wide spectrum of issues that can arise between a business and its insurer. When you’ve paid your premiums and held up your end of the deal, you expect your provider to do the same. An attorney steps in when they don’t, handling everything from initial claim filing support to complex litigation if the insurer refuses to pay what you are rightfully owed.

These lawyers focus on holding insurance companies accountable across several key practice areas. Whether your property was damaged in a storm, you were forced to close your doors temporarily, or you’re facing a lawsuit from a third party, a specialized attorney understands the specific challenges of commercial claims. They are prepared to manage the intricate details of your policy and fight for the full compensation your business deserves. They work exclusively for policyholders, not the insurance giants, so their only goal is to protect your interests. This focus is critical because insurance policies are notoriously complex, and insurers have teams of lawyers dedicated to minimizing payouts. Having an expert on your side levels the playing field.

Property damage claims

When your commercial property suffers physical damage from events like a fire, flood, hail, or windstorm, you turn to your policy for help. A commercial insurance claim dispute attorney assists clients with issues related to many types of commercial property insurance. Disputes often arise when the insurer undervalues the cost of repairs, argues that the damage isn’t covered, or delays payment without a valid reason. An attorney helps you document the full extent of your losses, interpret your policy’s coverage, and challenge an insurer’s unfair assessment to get the funds you need to rebuild and reopen.

Business interruption claims

Property damage often leads to a second, equally damaging problem: you can’t operate your business. Business interruption insurance is designed to cover lost income and operating expenses while your property is being repaired. However, insurers may dispute the length of the interruption or the amount of income you actually lost. They might push for a quick, lowball settlement that doesn’t truly cover your expenses. An attorney can help you accurately calculate and prove your losses, ensuring the insurance company provides the support needed to keep your business afloat during a difficult time.

Liability claims

Commercial general liability insurance is meant to protect your business if it’s accused of causing injury or property damage to someone else. For example, if a customer is injured on your premises (a premises liability claim), your policy should cover legal defense costs and any resulting settlement or judgment. Disputes happen when the insurance company refuses to defend you or denies coverage for the claim, leaving your business exposed to significant financial risk. An attorney can step in to enforce the insurer’s duty to defend and indemnify you, protecting your company’s assets and reputation.

Bad faith insurance practices

Sometimes, an insurer’s denial or delay isn’t just a disagreement; it’s a deliberate strategy. Insurance companies often act in bad faith when they use unreasonable tactics to avoid paying a valid claim. This can include refusing to investigate, intentionally misinterpreting policy language, making threatening statements to discourage you from pursuing your claim, or offering a settlement that is far below what you are owed. An attorney who handles bad faith cases can not only fight for your original claim benefits but also seek additional damages for the insurer’s wrongful conduct.

Why Do Insurance Companies Deny Commercial Claims?

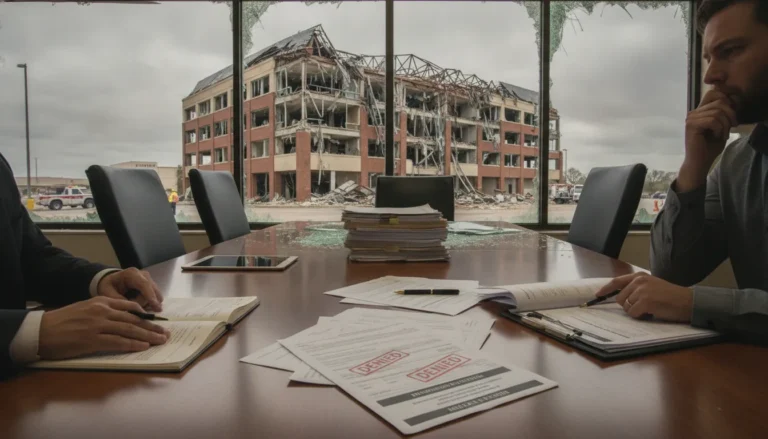

Receiving a denial letter after faithfully paying your premiums can feel like a profound betrayal. You held up your end of the bargain, but when you needed them most, your insurer said no. While some denials are based on legitimate policy terms, many are not. Insurance companies are for-profit businesses, and unfortunately, their financial interests can sometimes lead them to deny, delay, or underpay valid claims. Understanding the common reasons behind these denials is the first step in fighting back and getting the compensation your business deserves.

Confusing policy language and exclusions

Commercial insurance policies are dense, complex legal documents, not light reading. They are often filled with jargon, convoluted sentences, and long lists of exclusions that can be difficult for anyone without a legal background to understand. An insurer might deny your claim by pointing to a specific clause buried deep within your policy that they interpret in their favor. They may argue that your specific type of damage is excluded or that a particular condition wasn’t met. This is a common tactic used to discourage policyholders who may not have the expertise to challenge the insurer’s interpretation. A property insurance lawyer can level the playing field by translating this complex language and holding the insurer accountable to what the policy actually covers.

Lack of documentation

When you file a claim, the burden of proof is on you to demonstrate the extent of your losses. Insurance companies require extensive documentation, and any gaps can be used as a reason to devalue or deny your claim. For a busy business owner dealing with the aftermath of a fire, storm, or other disaster, gathering every single receipt, inventory list, and repair estimate is a monumental task. You need to provide clear evidence, including photos and videos of the damage, detailed lists of destroyed or damaged property with their values, and records of any expenses incurred due to the loss. Without meticulous records, the insurer can easily argue that you haven’t sufficiently proven your claim.

Missed deadlines or procedural mistakes

The insurance claims process is governed by strict deadlines outlined in your policy. You typically have a limited time to notify your insurer of a loss and an entirely separate deadline for submitting a formal, sworn document known as a “Proof of Loss.” Missing one of these deadlines by even a day can give the insurance company grounds for an automatic denial, no matter how valid your claim is. These procedural requirements are traps for the unwary. An insurer may not go out of their way to remind you of an approaching deadline, knowing that a simple mistake on your part can save them from having to pay the claim.

Lowball offers and underpayments

At the end of the day, insurance companies are businesses designed to generate profit. One of the most straightforward ways they do this is by paying out less in claims than they collect in premiums. This financial reality often leads to lowball settlement offers. An adjuster may contact you quickly after a loss, acting friendly and sympathetic while offering a fast payment. This offer is almost always less than what your claim is truly worth. They are counting on you being stressed and in need of cash to accept the low offer without a fight. This practice of undervaluing and underpaying claims is a key reason why having an experienced advocate who has achieved significant results for clients is so critical.

How an Attorney Fights for Your Business

When you’re facing a dispute with your insurance company, it can feel like you’re up against a wall. Insurers have teams of lawyers and adjusters working to protect their bottom line, which can leave you feeling overwhelmed and outmatched. Hiring an attorney levels the playing field. A commercial insurance lawyer doesn’t just send a few letters; they execute a strategic plan designed to get you the compensation your business is owed. This process is methodical and proactive, starting long before any courtroom appearance. It involves a deep dive into your policy to understand every detail, a meticulous collection of evidence to build an undeniable case, skilled negotiation to press for a fair settlement, and, if necessary, a powerful fight in court. It’s about having a dedicated advocate in your corner who understands the system and is committed to protecting your interests every step of the way. Let’s walk through exactly what a dedicated attorney does to champion your business’s claim and hold the insurance company accountable.

Decoding your insurance policy

Commercial insurance policies are notoriously dense and complicated documents, often filled with jargon and confusing clauses. An attorney specializing in property insurance claims starts by thoroughly analyzing your policy. They comb through every page to pinpoint the exact coverage you’re entitled to and identify any potential loopholes the insurer might try to exploit. This step is about more than just reading the fine print; it’s about interpreting the complex language of insurance law to understand your rights and the full extent of the insurer’s obligations to you. This foundational work sets the stage for the entire claim strategy.

Building your case with strong evidence

A strong insurance claim is built on a foundation of solid evidence. Your attorney will lead the effort to gather and organize everything needed to prove your case. This includes collecting documentation of your losses, such as repair estimates and financial records, as well as preserving all communications with the insurance company. They may also bring in independent experts, like engineers or public adjusters, to provide testimony that supports your claim. The goal is to construct a compelling and undeniable narrative that clearly shows the validity of your position and leaves no room for the insurer to unfairly deny or underpay you.

Negotiating with the insurance company

With a strong case built, an experienced attorney will engage in strategic negotiations with the insurance company on your behalf. They handle all communication, so you don’t have to deal with the stress of talking to adjusters. Leveraging their deep knowledge of Texas law and proven negotiation tactics, they will push for a fair settlement that covers your losses. An attorney who regularly handles property insurance disputes knows the insurance company’s playbook and can anticipate their arguments. This experience is crucial for resolving your claim efficiently and securing a favorable outcome without needing to go to trial.

Taking your case to court

If the insurance company refuses to negotiate in good faith or make a reasonable offer, your attorney must be ready to take the fight to court. A true trial lawyer, like Tim Hoch, prepares every case from the very beginning with the assumption that it might end up before a jury. This level of preparation not only ensures you’re ready for litigation but also puts maximum pressure on the insurer to settle fairly. In court, your attorney will advocate fiercely for your interests, presenting the evidence and making persuasive arguments to a judge and jury to secure the justice your business deserves.

Your Claim Was Denied. What’s Next?

Receiving a denial letter for your commercial insurance claim can feel like a final, frustrating end to a long process. But it’s important to know that a denial is not the last word. It’s the insurance company’s position, not a legal ruling. If you believe your claim is valid, this is the point where you shift from filing a claim to fighting for your rights. Taking a few strategic, immediate steps can protect your business and set the stage for a successful appeal or legal action. Think of the denial letter not as a closed door, but as the starting point for the real work ahead.

Read your denial letter closely

The first thing you need to do is carefully read the entire denial letter. The insurance company is required to provide a reason for its decision, and this letter is your first piece of evidence. Pay close attention to the specific policy language or exclusions they cite. Sometimes, the reasoning is buried in confusing jargon designed to make you give up. Insurers may even act in “bad faith,” which means they might refuse to pay a valid claim or create unnecessary hurdles. Understanding their stated reason is the first step in building your counter-argument with a Fort Worth property insurance lawyer.

Keep a record of everything

From this moment on, documentation is your best friend. Create a dedicated file for your claim and gather every single piece of paper and digital communication related to it. This includes your original insurance policy, all correspondence with the insurer (emails, letters), photos and videos of the damage, repair estimates, and a log of every phone call with dates, times, and who you spoke with. If you’re facing a dispute, you need to act quickly and save all documents. This organized record will become the foundation of your case and is critical for proving the facts. This level of diligence is what helps achieve positive results in complex disputes.

Don’t talk to the insurer alone

Once your claim is denied, you should avoid speaking directly with the insurance adjuster or company representatives by yourself. Remember, their job is to protect the company’s bottom line, not to help you. They are trained negotiators, and anything you say could be misinterpreted or used to justify their denial. Some companies are known to drag out cases for months or even years, hoping you’ll get frustrated and accept a lowball offer or abandon the claim entirely. Having an experienced attorney handle all communication ensures your rights are protected and that you don’t accidentally weaken your position.

Call an attorney as soon as possible

If your commercial claim has been denied, delayed, or underpaid, the single most effective step you can take is to contact an attorney who specializes in insurance disputes. Don’t wait. An experienced lawyer can immediately review your denial letter, analyze your policy, and explain your options. They take over the stressful communications with the insurer and begin building a case to get you the money you are owed. Having a board-certified trial lawyer like Tim Hoch on your side sends a clear message to the insurance company: you are serious about fighting for a fair outcome.

How to Prepare for Your First Consultation

Walking into an attorney’s office for the first time can feel intimidating, but it doesn’t have to be. Think of this initial consultation as your first strategy session. It’s a chance for you to interview the attorney and for them to get a clear picture of your situation. The more prepared you are, the more productive the meeting will be. You’re not just explaining what happened; you’re laying the groundwork for your case. A good attorney will listen, ask clarifying questions, and give you an honest assessment of your options. Your goal is to leave the meeting with a clear understanding of the path forward and confidence that you have a strong advocate in your corner.

What to bring to your first meeting

To make the most of your consultation, gather every piece of paper and digital file related to your claim. Don’t worry about organizing it perfectly; just bring it all. Your attorney is skilled at sifting through documents to find what matters. Your collection should include your complete insurance policy (including all declarations and endorsements), the denial or underpayment letter from your insurer, and a full record of your communication with them. Also, bring any photos or videos of the damage, repair estimates you’ve received, and financial records that show business losses. Having these materials on hand helps an attorney give you a more accurate initial assessment of the practice areas involved in your case.

Key questions to ask the attorney

This meeting is a two-way street, so come with questions. You are hiring a professional to protect your business, and you need to be sure it’s the right fit. Start by asking about their specific experience with commercial insurance disputes in Texas. You can ask, “How many cases like mine have you handled?” or “What were the outcomes?” Inquire about who your primary point of contact will be and how the firm communicates updates. It’s also wise to ask about their trial experience. An attorney who regularly takes cases to court, like Tim Hoch, often gets better settlement offers because insurers know they aren’t afraid to fight.

Understanding the process ahead

A good attorney will use this first meeting to outline what you can expect in the coming weeks and months. They should explain the initial steps, which usually involve a deep dive into your policy and a formal communication with the insurance company. Ask them to walk you through the potential timeline, from negotiation and mediation to what happens if a lawsuit becomes necessary. They should also clearly explain their fee structure. Most reputable property insurance attorneys work on a contingent fee basis, meaning you don’t pay unless they recover money for you. Understanding this process from the start helps manage your expectations and builds a foundation of trust for the fight ahead.

Will an Attorney Actually Speed Up My Claim?

It’s a frustrating situation. You’ve been paying your premiums faithfully, but now that you need to file a claim, the insurance company is moving at a glacial pace. It’s natural to wonder if bringing in a lawyer will add more time and complexity to an already slow process. The short answer is that while every case is different, an experienced attorney can often break through the delays and get things moving.

When you hire a lawyer, the dynamic with your insurance company changes immediately. The insurer knows they can no longer use the same stall tactics on you. An attorney speaks their language, understands the legal deadlines they must meet, and can apply pressure in ways a policyholder simply can’t. Suddenly, your claim is no longer just another file at the bottom of the pile; it’s a legal matter that demands a timely and serious response.

A huge reason claims get delayed is because of disorganized or incomplete information. An experienced property insurance lawyer prevents this by building a thorough and professional claim from the very beginning. They gather all the necessary evidence, document your losses meticulously, and present a comprehensive package to the insurer. This level of preparation leaves the insurance company with fewer excuses to request more information or drag out the review process.

Ultimately, an attorney’s involvement is about efficiency and leverage. They can cut through the red tape and negotiate directly with the people who have the authority to approve your claim. If the insurer is using intentional delays as one of their bad faith tactics, your attorney can call them on it and take legal action to compel a response. While the goal is always a fair and efficient resolution, a good attorney prioritizes the best outcome over the fastest one. They won’t let you accept a quick lowball offer just to close the case. They fight to get you the full compensation you deserve, even if it means the process takes a little longer to get right.

Finding the Right Commercial Insurance Attorney in Texas

When your business is on the line, choosing the right legal partner is one of the most important decisions you’ll make. Your insurance company has a team of lawyers, and you deserve an expert advocate in your corner. But how do you find the right one? Look for an attorney with a specific set of qualifications that demonstrate they have what it takes to stand up to major insurance carriers and fight for your business.

Prioritize proven trial experience

Insurance companies are powerful institutions, and they know which attorneys are willing to go to trial and which ones prefer to settle quickly. An attorney with a strong track record in the courtroom brings a level of leverage to the negotiating table that can’t be faked. Their willingness to see a case through to a verdict often results in better settlement offers because the insurer wants to avoid the risk and expense of a trial they might lose. When you vet a potential lawyer, ask about their trial experience and their history of results. As the State Bar of Texas notes, trial experience is essential for an attorney to advocate effectively for their clients in court.

Check for board certifications

Board certification is a significant mark of distinction for any attorney in Texas. It’s a voluntary designation that signals an exceptional level of skill and expertise in a specific area of law. To become board-certified, an attorney must have extensive experience, receive positive reviews from peers and judges, and pass a rigorous day-long exam. According to the Texas Board of Legal Specialization, less than 10% of licensed Texas attorneys are board-certified. When an attorney like Tim Hoch is Board Certified in Personal Injury Trial Law, it confirms he has the highest level of proven trial competence, a critical skill when battling an insurance company on your behalf. You can always verify an attorney’s certification online.

Understand their contingency fee

The cost of legal representation is a valid concern for any business owner. That’s why many of the best commercial insurance attorneys work on a contingency fee basis. In simple terms, this means you pay no attorney’s fees unless they successfully recover money for you. The attorney’s fee is a percentage of the final settlement or verdict, which aligns their interests directly with yours: they are motivated to maximize your recovery. This arrangement allows you to secure top-tier legal help without any upfront cost or financial risk. Before signing, make sure you receive a clear, written agreement that outlines the percentage and how case expenses are handled.

Red flags to watch for when hiring

Just as there are signs of a great attorney, there are also red flags that should give you pause. Be wary of any lawyer who guarantees a specific outcome, as no ethical attorney can promise a win. A lack of communication is another major warning sign; if they are difficult to reach or vague in their answers from the start, that pattern is likely to continue. You should also be cautious if an attorney is not transparent about their fee structure or seems hesitant to discuss their experience with cases like yours. Your attorney should be a trusted partner, so if your gut tells you something is off, it’s best to keep looking.

Related Articles

- Should You Hire an Attorney for Insurance Claim Denial?

- How to Find the Best Lawyer for a Denied Commercial Claim

- How a Commercial Insurance Claim Denial Lawyer Can Help

- When to Hire a Fort Worth Underpaid Commercial Claim Attorney

- When to Hire a Business Insurance Claim Litigation Attorney

Frequently Asked Questions

I’m worried about legal fees. How can my business afford an attorney when we’re already facing losses? This is a completely valid concern, and it’s one of the biggest reasons to look for an attorney who works on a contingent fee basis. This payment structure means you don’t pay any attorney’s fees upfront. Instead, the lawyer’s fee is a percentage of the money they successfully recover for you. If they don’t win your case, you don’t pay them a fee. This approach allows your business to get expert legal help without any financial risk, and it ensures your attorney is just as motivated as you are to get the best possible result.

Should I wait for my claim to be denied before I contact an attorney? While a denial letter is a definite sign that you need legal help, you don’t have to wait for one. If your claim is particularly large or complex, or if you feel the insurance company is already giving you the runaround with delays and endless requests for information, it’s smart to consult an attorney. Getting a lawyer involved early can prevent you from making procedural mistakes and can often get the claim on the right track from the start, saving you time and stress down the road.

My insurance company offered a settlement, but it feels low. Is it worth hiring an attorney just to get a little more? That low offer is a common tactic. Insurers often count on you being stressed and needing cash quickly, so they offer a fast payment that is much less than what you’re actually owed. The difference between that initial offer and the true value of your claim can be significant, sometimes covering the cost of repairs or lost income that the insurer conveniently overlooked. An experienced attorney can assess the full scope of your losses and determine what a fair settlement really looks like. It’s often not about getting “a little more,” but about getting the full amount your policy was meant to provide.

If I hire an attorney, do I lose control over the decisions in my claim? Not at all. Hiring an attorney means you are bringing a professional advocate onto your team, not giving up your authority. Your lawyer will handle the stressful communications, manage the legal complexities, and advise you on the best strategy. However, you are still the client. All major decisions, especially the crucial one of whether to accept a settlement offer, remain yours to make. A good attorney keeps you informed and empowered throughout the entire process.

I already have a business lawyer I trust. Why do I need a different attorney just for an insurance claim? It’s great that you have a trusted legal advisor. Think of it this way: you’d see a cardiologist for a heart issue, not just your family doctor. Insurance law is a highly specialized field with its own complex rules and procedures. An attorney who focuses exclusively on representing policyholders against insurance companies understands the specific tactics insurers use to deny and underpay claims. They live and breathe this area of law and have the focused experience needed to effectively fight for your business.

For tailored guidance on a disputed or high-value claim, speak with a Fort Worth commercial insurance dispute attorney before important deadlines or evidence issues narrow your options.