Facing off against a major insurance corporation can feel like an impossible battle. They have vast resources, teams of adjusters, and lawyers dedicated to minimizing payouts. As a property owner, it’s easy to feel outmatched and pressured into accepting an unfair settlement. But you don’t have to go through this alone. The key is to level the playing field with an advocate who knows the insurer’s playbook and isn’t afraid to challenge them. Hiring the right office building insurance dispute lawyer sends a clear message: you are serious about getting the full and fair compensation you are owed and are prepared to fight for it.

Key Takeaways

- Hire a specialist for a strategic advantage: A dedicated property insurance lawyer does more than just file paperwork; they manage the entire claims process, from accurately valuing your damages to handling all communication with the insurer, giving you a powerful advocate from the start.

- Control the narrative with documentation: Your best tool is a strong case built on evidence, so meticulously photograph all damage, keep a detailed log of every conversation with your insurer, and be careful with your words, as casual comments can be used to weaken your claim.

- Treat a denial as a starting point, not an ending: An initial denial or lowball offer is often a negotiation tactic. Always get the insurer’s decision in writing, obtain independent repair estimates, and consult an attorney before accepting any settlement.

How Can an Office Building Insurance Lawyer Help You?

When you’re facing a significant loss at your commercial property, a dispute with your insurance company is an unwelcome burden. An experienced office building insurance lawyer acts as your dedicated advocate, managing the complex legal and financial details so you can focus on your business. They build a strategic case to protect your rights at every turn. From deciphering your policy to taking your case to court, their support can be the deciding factor in reaching a fair outcome.

An attorney’s involvement goes beyond just sending letters. They conduct an independent investigation, document the full scope of your damages, and bring in a network of trusted experts like engineers and public adjusters to create an accurate valuation of your claim. This proactive approach ensures you have a solid, evidence-based argument from the start. They handle all the stressful back-and-forth with the insurer, shielding you from pressure tactics and confusing requests. By managing the entire process, they allow you to get back to what you do best: running your business. Their expertise is particularly valuable when claims are complex, involving multiple types of damage or significant business interruption losses that insurers often try to minimize.

Breaking Down Your Policy and Valuing Your Claim

Your commercial property policy is a complex legal contract filled with confusing language and hidden exclusions. Trying to interpret it alone after a disaster can lead to costly mistakes. A skilled property insurance lawyer will analyze your policy to determine the full extent of your coverage. They identify every potential source of recovery, from structural repairs to business interruption and lost rental income. This detailed valuation is critical; it establishes a fact-based foundation for your claim and prevents you from accepting an offer that doesn’t cover your true losses.

Handling Negotiations, Appeals, and Lawsuits

Dealing with an insurance company can feel like an uphill battle. Their adjusters and legal teams are trained to protect the company’s bottom line. When you hire an attorney, you level the playing field. Your lawyer takes over all communications, presenting your claim professionally and shielding you from pressure tactics. If your claim is unfairly denied, they will manage the appeals process. Should the insurer refuse to negotiate in good faith, your attorney will be prepared to file a lawsuit and advocate for you in court.

The Difference Between a General Attorney and a Specialist

While many attorneys handle contract disputes, property insurance law is a highly specialized field. A general practice lawyer may not know the specific statutes governing insurance claims in Texas or the tactics insurers use to deny payment. A specialist, particularly a Board Certified trial lawyer, brings a deeper level of knowledge. They understand the nuances of insurance litigation, have relationships with trusted experts like engineers, and know how to build a case that can withstand courtroom scrutiny. Choosing a specialist ensures you have an advocate who truly understands the fight ahead.

Common Insurance Hurdles for Texas Office Building Owners

As a Texas office building owner, you know that having the right insurance policy is a fundamental part of protecting your investment. You pay your premiums on time and trust that your provider will be there for you when you need them. However, when you actually have to file a claim, you might find that the process is far from simple. Insurance companies are businesses, and their goal is to minimize payouts. This can lead to a number of frustrating and financially damaging roadblocks for property owners trying to recover after a loss.

From navigating the aftermath of a severe storm to fighting for the full value of your repairs, the path to a fair settlement is often filled with obstacles. Insurers may use complex policy language, questionable damage assessments, and delay tactics to wear you down. Understanding these common hurdles is the first step in protecting your rights and ensuring you get the compensation you deserve. It’s important to remember that you don’t have to face these challenges alone; knowing when to bring in a legal professional can make all the difference in your case.

Claims for Property and Storm Damage

Texas is no stranger to severe weather. Hailstorms, tornadoes, and hurricanes can cause devastating damage to commercial properties in an instant. While you might think filing a claim for storm damage would be straightforward, it’s often the beginning of a long and complicated process. The Texas Department of Insurance notes that our state is particularly prone to these events, which leads to a high volume of claims. Insurers may try to argue that the damage was pre-existing or caused by something not covered under your policy, like flooding instead of wind. They might also dispute the date of the loss, making it difficult to prove your case without meticulous documentation and a clear understanding of your policy’s terms.

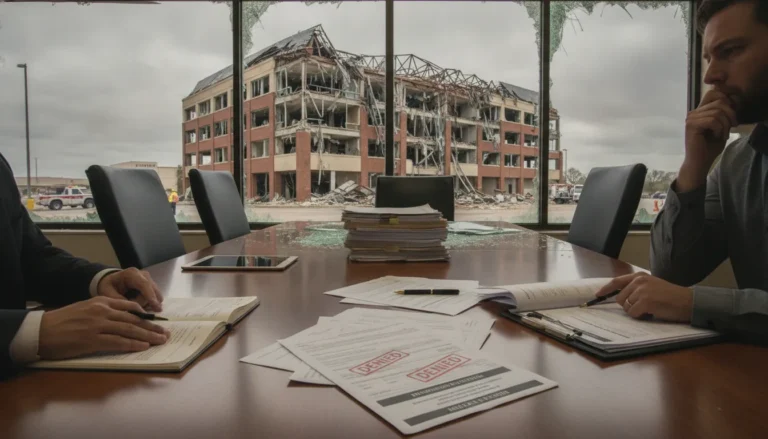

Facing Unfair Denials or Lowball Offers

One of the most disheartening experiences for a property owner is receiving an outright denial or a “lowball” settlement offer that doesn’t come close to covering the cost of repairs. According to the National Association of Insurance Commissioners, insurers may deny claims based on technicalities or policy exclusions that are buried in the fine print. They might also send an adjuster who is trained to minimize the scope of the damage, resulting in an offer that leaves you to pay for a significant portion of the repairs out of pocket. These tactics are designed to protect the insurance company’s bottom line, not to help you recover from your loss.

Arguing Over the True Cost of Damage

Even if your insurer agrees to cover the claim, disputes over the cost of repairs are incredibly common. Your contractor provides a detailed estimate for restoring your property, but the insurance company’s adjuster comes back with a much lower number. This often happens because the insurer’s estimate may use cheaper materials, overlook certain types of damage, or fail to account for local labor costs. The Insurance Information Institute highlights that these disagreements can lead to lengthy delays, leaving your property vulnerable to further damage while you argue over the proper valuation. This stalemate can put your business operations on hold and create immense financial strain.

When Your Insurer Acts in Bad Faith

Sometimes, an insurer’s conduct goes beyond simple disputes and crosses the line into bad faith. This occurs when an insurance company fails to uphold its contractual obligations by engaging in deceptive or unfair practices. Examples include unreasonably delaying the investigation or payment of a valid claim, refusing to provide a reason for a denial, or misrepresenting the terms of the policy. When an insurer acts in bad faith, they are not just breaching a contract; they are violating the law. If you suspect your insurance company is intentionally trying to avoid paying what they owe, it is crucial to speak with a Fort Worth property insurance lawyer who can hold them accountable.

Avoid These Common Mistakes with Your Insurance Claim

After your office building suffers damage, the last thing you want is a drawn-out battle with your insurance company. Unfortunately, the claims process is full of potential missteps that can jeopardize your financial recovery. Being aware of these common mistakes is the first step toward protecting your interests and getting the full amount you’re owed. Let’s walk through what to watch out for.

Not Documenting Enough or Reporting Too Late

Time is not on your side after a storm or other incident damages your property. Most insurance policies have strict deadlines for reporting a claim, sometimes as short as 30 days. Waiting too long can give the insurer a reason to deny your claim outright. Just as important is documenting everything. Before you clean up, take extensive photos and videos of all the damage from multiple angles. Keep a detailed log of every conversation with the insurance company, and save all receipts for repairs or temporary relocation costs. This evidence is your best tool for proving the full extent of your loss and holding your insurer accountable.

Misinterpreting Your Policy’s Fine Print

Insurance policies are notoriously dense and filled with legal jargon. It’s easy to get lost in the fine print, and it’s common for honest disagreements to arise over what your policy actually covers. You might think a certain type of damage is included, only to have the adjuster point to an obscure exclusion clause. This is not a personal failure; these documents are designed to be complex. An experienced Fort Worth property insurance lawyer can interpret the specific language of your policy, identify your rights, and make sure the insurance company honors its obligations. Don’t let confusing language stand between you and a fair settlement.

Underestimating the Full Extent of Your Damages

Never assume the insurance company’s initial assessment of your damages is accurate. Their goal is to pay out as little as possible, and their adjusters are trained to minimize the scope of your loss. They might overlook hidden structural damage, undervalue the cost of materials, or offer a lowball settlement hoping you’ll take it and move on. It’s crucial to get your own independent estimates from trusted contractors. A thorough attorney will often bring in their own network of experts to build a comprehensive valuation of your claim, ensuring nothing is missed. The firm’s track record of results often speaks to their ability to fight for a claim’s true value.

Saying the Wrong Thing to Your Insurer

It’s important to remember that the insurance adjuster is not your friend. They work for the insurance company, and their job is to protect the company’s bottom line. Anything you say in a recorded statement or even a casual phone call can be twisted and used to deny or reduce your claim. A simple comment like, “The roof was getting old anyway,” could be used to argue the damage was due to wear and tear, not the storm. It’s best to keep your communication with the adjuster brief, factual, and in writing. Better yet, let an attorney like Tim Hoch handle the communication for you, as he knows exactly how to speak to insurers to protect your rights from the start.

What to Do If Your Office Building Insurance Claim Is Denied

Receiving a denial for your office building insurance claim can feel like a major setback, but it’s not the end of the road. It’s easy to feel frustrated and even defeated when the company you’ve paid for protection turns its back on you. However, it’s important to see this moment for what it is: the start of a new phase in the claims process, one where you take control. How you respond in the moments and days after a denial can significantly shape your final outcome. Taking a few strategic, deliberate steps can protect your rights and put you in a much stronger position to challenge the insurer’s decision.

This is your opportunity to shift from reacting to the insurance company’s moves to proactively managing your claim. The initial denial is the insurer’s first move, not the final word. Many valid claims are initially denied or undervalued. By understanding the process and your rights, you can effectively counter their decision. It’s about methodically building your case, gathering the right documentation, and knowing when to bring in professional help. This approach allows you to fight for the full and fair compensation you’re owed for your property, turning a potential dead end into a path toward recovery.

Get the Denial in Writing

If your insurance company denies your claim over the phone, your first step is to request that they send you the denial in a formal letter. A verbal denial isn’t enough. You need an official document that clearly states the specific reasons for their decision, referencing the exact parts of your policy they believe support their position. This letter is a critical piece of evidence. It becomes the foundation for your appeal and allows a property insurance lawyer to analyze the insurer’s argument and identify any weaknesses or misinterpretations of your coverage. Don’t move forward until you have this letter in hand.

Keep a Detailed Record of Everything

From the moment you notice the damage, you should be documenting everything. If you haven’t started, begin now. Create a comprehensive file that includes photos and videos of the damage from multiple angles, a detailed inventory of all damaged property with estimated values, and copies of any receipts for temporary repairs. Just as important, keep a communication log. Every time you speak with someone from the insurance company, write down their name, the date and time of the call, and a summary of what was discussed. This meticulous record-keeping creates a clear timeline and provides the concrete evidence needed to support your claim.

Don’t Settle for a Lowball Offer

Insurance companies sometimes follow up a denial with a lowball settlement offer, hoping you’ll feel pressured enough to accept a fraction of what you need. It’s important to remember that their first offer is rarely their best one. These initial offers often fail to account for the full scope of repairs, business interruption costs, and other expenses. Don’t accept an offer or sign any releases until you are confident it covers all your losses. It’s always wise to have an independent contractor assess the damage and get a legal opinion on the offer to ensure it’s fair. Seeing the results a skilled attorney can achieve often highlights the inadequacy of these first offers.

Talk to a Property Insurance Attorney—Sooner Than Later

The insurance adjuster may seem friendly, but their job is to protect the insurance company’s bottom line, not yours. The best way to level the playing field is to have an expert on your side. Contacting a property insurance attorney as soon as you run into trouble can make all the difference. An experienced lawyer can take over communications with the insurer, manage the appeals process, and build a compelling case on your behalf. A board-certified trial lawyer like Tim Hoch brings a level of expertise that shows the insurance company you are serious about defending your rights and prepared to go to court if necessary.

What to Look for in an Office Building Insurance Dispute Lawyer

When you’re fighting an insurance company over your office building claim, the lawyer you choose can make all the difference. Your property is a significant investment, and you need an advocate who has the right skills and experience to protect it. Not all attorneys are equipped to handle these complex disputes. Look for a lawyer with a specific set of qualifications that signal they are ready to take on a powerful insurance carrier and fight for the compensation you deserve.

Look for Trial Experience and Board Certification

Insurance companies are well aware of which lawyers are willing to take a case to court and which ones prefer to settle quickly. An attorney with a proven track record in the courtroom has significant leverage during negotiations. When your lawyer is a known trial threat, insurers are often more willing to offer a fair settlement from the start. Beyond that, look for a lawyer who is Board Certified. This distinction is earned by a small percentage of attorneys and signifies a deep level of expertise and commitment to a specific area of law, ensuring you have a true specialist on your side.

Find Someone with Strong Negotiation Skills and Expert Resources

A successful outcome often hinges on your lawyer’s ability to negotiate effectively. A skilled attorney knows how to communicate with insurance companies to secure a fair settlement without backing down. They also understand that a strong case is built on solid evidence. That’s why it’s important to find a property insurance lawyer who has access to a network of trusted industry experts. These professionals, like engineers and public adjusters, can provide crucial analysis to accurately value your claim and counter the insurance company’s assessments, strengthening your position at the negotiating table.

Choose a Firm That Offers a Contingency Fee and Personalized Service

Dealing with property damage is stressful enough without worrying about how to afford legal help. Look for a firm that offers its legal representation on a contingency fee basis. This arrangement means you don’t pay any attorney fees unless they successfully recover money for you. It makes quality legal help accessible and ensures your lawyer is motivated to get you the best possible result. You should also seek out personalized service. At a firm where you have direct contact with your attorney, you can be confident that your case is getting the attention it deserves from someone who understands your unique situation and goals.

Related Articles

- Why You Need an Office Building Property Damage Lawyer Texas

- Commercial Property Insurance – Hoch Law Firm, PC

- Commercial Property Insurance Claims Attorney | Hoch Law Firm, PC

- Find the Best Lawyer for Apartment Insurance Claims

- 5 Signs You Need an Apartment Complex Insurance Claim Lawyer

Frequently Asked Questions

When is the right time to contact an office building insurance lawyer? You don’t have to wait for an official denial to seek legal advice. If you feel that the insurance company is delaying the process, asking confusing questions, or making an offer that seems far too low, it’s a good time to talk to an attorney. An early consultation can help you avoid common mistakes and protect your rights from the very beginning, putting you in a much stronger position.

I’m already losing money from the property damage. How can I afford to hire a lawyer? This is a very common and understandable concern. Many specialized property insurance law firms, including ours, work on a contingency fee basis. This means the firm fronts the costs of building your case, and you do not pay any attorney fees unless they successfully recover money for you. This approach makes expert legal help accessible and ensures your lawyer is fully invested in achieving the best possible outcome for your claim.

My insurance claim was denied. Can’t I just handle the appeal process on my own? While you certainly have the right to appeal a decision yourself, it can be an uphill battle. Insurance companies have teams of legal experts dedicated to defending their denials. When you hire an attorney who specializes in property insurance disputes, you get an expert who understands the insurer’s tactics, can interpret complex policy language, and knows how to build a compelling legal case. It levels the playing field and signals to the insurance company that you are serious about fighting for what you’re owed.

The insurance adjuster seems helpful. Why shouldn’t I just work with them directly? It’s important to remember the adjuster’s role. While they may be perfectly pleasant, their primary professional duty is to their employer, the insurance company. Their goal is to resolve your claim in a way that protects the company’s financial interests, which often means paying out as little as possible. Anything you say can be used to limit your claim, so having an attorney manage all communications ensures your rights are the top priority at all times.

What is the first thing a lawyer will do after I hire them for my claim? Typically, the first step is a deep dive into your case file. Your lawyer will conduct a thorough review of your insurance policy, the damage reports, your communication log, and the insurer’s denial letter. From there, they will give you a clear assessment of your legal options. They will then formally notify the insurance company that they are representing you and take over all future communications, immediately relieving you of that burden and pressure.