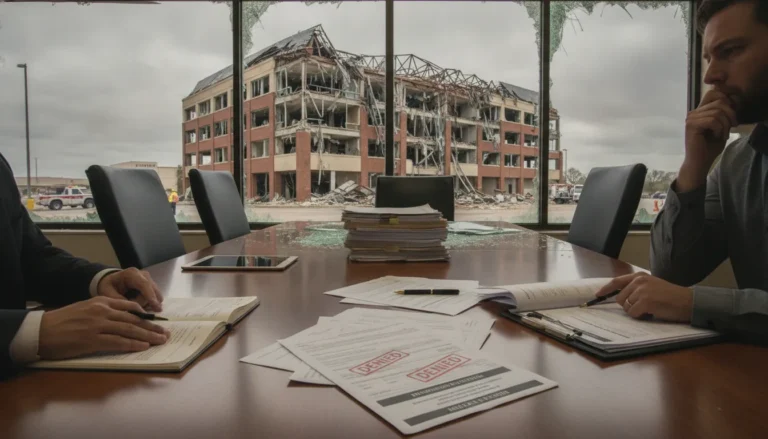

When you file a commercial insurance claim, you’re not entering a partnership; you’re entering a negotiation. Your insurance company has a team of adjusters, analysts, and lawyers all working with one primary goal: to minimize the company’s financial payout. They handle thousands of claims and know the process inside and out. As a business owner, you are at an immediate disadvantage. You are trying to run your business and recover from a disaster while facing a team of professionals on the other side. Hiring an underpaid commercial insurance claim lawyer is not about being aggressive; it’s about leveling the playing field. This guide will show you the red flags that indicate you need professional help and explain how the right attorney can advocate for you, ensuring your claim is valued fairly.

Key Takeaways

- Build your case before you file: Proactively protect your business by creating a detailed asset inventory and understanding your policy’s terms now. After a loss, get an independent damage assessment to counter the insurer’s low estimate and establish the true cost of recovery.

- Challenge the insurer’s numbers: Do not automatically accept the first offer, as insurers often use tactics like undervaluing materials or misinterpreting policy language to reduce payouts. Always demand a detailed written explanation for their valuation.

- Partner with an expert to level the playing field: You do not have to fight the insurance company alone. Hiring a commercial insurance lawyer on a contingency fee basis gives you a professional advocate to manage negotiations and fight for a fair settlement without upfront costs.

Is Your Commercial Insurance Claim Underpaid?

After a storm, fire, or other disaster damages your business, you expect your insurance company to step up. You’ve paid your premiums, and now you need the support you paid for to get back on your feet. So, when a check arrives that barely covers a fraction of the repair costs, it’s more than just disappointing; it’s a serious threat to your business. Unfortunately, this happens all the time. An underpaid claim isn’t just a low offer, it’s a tactic some insurers use to protect their profits. Recognizing the signs of underpayment is the first step toward fighting for the full amount your business is rightfully owed.

How Insurance Companies Underpay Claims

Insurance companies are businesses, and one way they increase profits is by minimizing payouts. This can show up in several ways during your claims process. An adjuster might conduct a rushed inspection, overlooking significant damage that isn’t immediately obvious. They may also create an estimate that uses cheaper materials or lower labor costs than what is realistically required for a quality repair. Another common tactic involves devaluing your property by applying heavy depreciation, paying you for the item’s old, worn-out value instead of what it costs to replace it. These are common strategies in property insurance disputes that can leave you with a huge financial gap.

Common Excuses Insurers Use to Underpay

When an insurance company makes a low offer, they usually have a justification ready. You might hear that their estimating software produced the number, but these programs are often designed to generate lowball figures. They hope you’ll be too overwhelmed to fight and will simply accept the first offer, signing away your right to seek more. Sometimes, the insurer will turn the tables and blame you, claiming you didn’t provide enough documentation for your losses or made a mistake on a form. While it’s crucial to be thorough, these can also be excuses to delay and underpay. A Fort Worth property insurance lawyer can help you see through these excuses.

Costly Policy Misinterpretations

Insurance policies are dense, complicated documents filled with legal jargon. Insurers can use this complexity to their advantage. An adjuster might tell you that a certain type of damage isn’t covered by your policy, even when it is. They may point to an exclusion that they interpret broadly or a provision that they interpret narrowly, all in an effort to limit the payout. Just because an adjuster says something isn’t covered doesn’t make it true. Getting an expert analysis of your policy is critical to understanding your rights and challenging these costly misinterpretations across all practice areas of insurance law.

The Real Impact of an Underpaid Claim on Your Business

When your business suffers damage from a storm, fire, or another disaster, the insurance check is supposed to be the lifeline that gets you back on your feet. But what happens when that check doesn’t even come close to covering the actual cost of your losses? An underpaid claim isn’t just an inconvenience; it’s a direct threat to your company’s stability and future. The shortfall creates a ripple effect, turning a manageable crisis into a long-term financial struggle that can impact everything from your daily operations to your ability to grow.

This is a scenario countless Texas business owners face. Insurance companies are focused on their bottom line, and sometimes that means their initial offer is based on a rushed inspection, a misunderstanding of your policy, or an undervaluation of your repair costs. They might pay for an item’s depreciated value instead of its replacement cost, argue that certain damages aren’t covered at all, or offer too little for labor and materials. For you, the result is the same: a staggering gap between what you were paid and what you actually need to recover. This gap can force you to make impossible choices that put the business you’ve worked so hard to build at risk.

Revenue Loss and Operational Headaches

An underpaid claim immediately disrupts your ability to do business. If you don’t have enough funds to complete repairs or replace essential equipment, you can’t operate at full capacity, if at all. Every day your doors are closed or your services are limited, you’re losing revenue while your regular expenses keep piling up. This financial pressure creates a cascade of operational headaches. You’re left scrambling to find contractors willing to work for less, sourcing cheaper materials that might not last, and spending your valuable time arguing with adjusters instead of serving your customers. These are not just minor frustrations; they are significant obstacles that can halt your business in its tracks, all because an insurer decided to underpay your claim.

Long-Term Financial Damage

The immediate cash crunch from an underpaid claim often leads to lasting financial harm. To cover the repair deficit, you might be forced to drain your business reserves, take out high-interest loans, or even use personal funds. This debt can strain your company’s finances for years, making it harder to invest in growth or weather future economic downturns. Accepting a lowball offer can also set a dangerous precedent, as you may be signing away your right to seek further compensation. Shoddy, incomplete repairs can decrease your property’s value and lead to more significant problems down the road. Protecting your business means understanding all your options before you agree to a settlement, which is why exploring your legal practice areas can provide clarity and a path forward.

What to Do If Your Commercial Claim Is Underpaid

Discovering your insurance company has underpaid your commercial property claim can feel like a second disaster. You’ve paid your premiums faithfully, and now, when you need support the most, the offer falls short of what’s needed to get your business back on its feet. Don’t accept a lowball offer as the final word. You have options and the right to fight for the full amount you are owed. Taking a few strategic steps can make all the difference in securing a fair settlement and protecting your business’s future.

Review Your Policy and Document Everything

First, go back to your insurance policy. This document is your contract with the insurer, and you need to understand exactly what it says about your coverage, limits, and exclusions. It can be dense, but knowing your policy is the foundation for a strong dispute. At the same time, document everything related to your damages and the claims process. Keep a detailed log of every phone call, email, and letter you exchange with the insurance company. Take photos and videos of the damage from multiple angles, and save all receipts for any temporary repairs or related business expenses you incur.

Get an Independent Assessment of Your Damages

Your insurance company’s adjuster works for them, not for you. Their goal is often to minimize the payout. To counter their low estimate, it is essential to get an independent assessment of your damages. Hire a trusted public adjuster, contractor, or engineer who can provide a detailed, line-by-line estimate of what it will actually cost to repair or rebuild your property. This third-party evaluation gives you a realistic number to work with and serves as powerful evidence to support your argument that the claim was underpaid.

Demand a Detailed Explanation From Your Insurer

If the insurer’s offer seems too low, don’t just accept it. You have the right to ask for a complete and detailed explanation of how they arrived at their number. Ask the adjuster to provide the specific policy language they are using to justify their valuation and to break down their estimate. This forces them to put their reasoning in writing, which can expose flaws in their assessment, misinterpretations of your policy, or bad faith tactics. A clear paper trail is your best friend in an insurance dispute.

Don’t Give a Recorded Statement Without Your Lawyer

Insurance adjusters will often ask you to provide a recorded statement about the damage. Be very careful. They are trained to ask questions in a way that can get you to say something that hurts your claim. You might accidentally downplay the damage or misremember a small detail that they can later use to question your credibility. It is always best to politely decline to give a recorded statement until you have spoken with an experienced Fort Worth property insurance lawyer who can advise you on how to protect your rights.

File a Formal Appeal or Supplemental Claim

A low initial offer is not the end of the process. You can formally appeal the insurance company’s decision. You can also file a supplemental claim to introduce new information, such as the independent damage assessment you obtained. This reopens the discussion and shows the insurer you are serious about getting the full amount you are owed. Even if your claim was already closed, you can often reopen it if you discover the initial payment was not enough to cover the full cost of repairs. This is a critical step where having legal guidance can be invaluable.

When to Hire a Commercial Insurance Claim Lawyer

You’ve followed all the rules. You documented the damage, filed your claim promptly, and provided every piece of information your insurer requested. Yet, the settlement offer that landed in your inbox is a fraction of what you actually need to repair your property and get your business running again. It’s a frustrating and deeply unfair position to be in. While you can try to appeal the decision on your own, there comes a point when you need to bring in a professional.

Hiring a lawyer isn’t about starting a fight; it’s about leveling the playing field. Your insurance company has a team of adjusters and attorneys working to protect its bottom line. Their goal is often to pay out as little as possible. An experienced commercial insurance claim lawyer works for you and only you. They understand the complex language in your policy and the common tactics insurers use to underpay claims. Bringing an attorney into the process sends a clear message that you are serious about getting the full and fair payment your business is owed. They can take over the stressful communications and build a strong case on your behalf, letting you focus on what you do best: running your business.

Red Flags That You Need Legal Help

Trust your gut. If the insurance company’s offer feels wrong, it probably is. Insurers often count on you not knowing the true value of your claim. If you suspect your claim has been underpaid, it’s time to get a second opinion from a legal expert. Other clear signs that you need help include the insurer blaming you for the damage, misinterpreting your policy language to deny coverage, or dragging their feet for weeks or months without a clear reason. These are common strategies used to wear you down until you accept a lowball offer. An attorney who handles insurance disputes will recognize these tactics immediately and know exactly how to respond.

Why Acting Quickly Matters in Texas

After your claim is underpaid, the clock starts ticking. Texas has strict deadlines, known as statutes of limitations, for filing a lawsuit against an insurance company. If you miss this window, you could lose your right to recover the money you are owed, no matter how strong your case is. Acting quickly also helps preserve crucial evidence and witness memories. The longer you wait, the more challenging it becomes to prove the full extent of your damages. A Fort Worth property insurance lawyer can immediately take steps to protect your rights and ensure all deadlines are met. Even if some time has passed, don’t give up. It may still be possible to reopen a claim, so it’s always worth getting a professional evaluation of your situation.

What Will a Commercial Insurance Claim Lawyer Do for You?

When you’re facing a massive disruption to your business, the last thing you need is a fight with your insurance company. Hiring a commercial insurance claim lawyer is about bringing in a professional to manage that fight for you. Think of it this way: you’re an expert at running your business, and they are experts at holding insurance companies accountable. Their entire job is to take the weight of the claims process off your shoulders and level the playing field.

An experienced attorney acts as your advocate and project manager. They handle the complex paperwork, the frustrating phone calls, and the tough negotiations, all while building a powerful case for the full amount you are owed. This allows you to focus on what matters most: keeping your business operational. From the moment you hire them, they work to protect your rights and ensure the insurance company honors its promises, giving you the peace of mind that a professional is fighting for your business’s future.

Analyze Your Policy and Maximize Coverage

One of the first things a lawyer will do is conduct a deep dive into your commercial policy. These documents are often dense, confusing, and filled with technical language designed to limit coverage. Your attorney will review your insurance policy to identify every possible source of coverage for your losses, including things an adjuster might have conveniently overlooked. They understand the nuances of Texas insurance law and how specific clauses should be interpreted in your favor. This thorough analysis ensures that you are claiming the maximum benefits available, setting a strong foundation for the entire claims process and preventing the insurer from unfairly limiting your recovery from the start.

Bring in Experts to Assess the True Damage

Your insurance company will send its own adjuster to assess the damage, but their goal is often to minimize the payout. To counter this, your lawyer will assemble a team of independent experts to determine the true scope and cost of your loss. This team may include structural engineers, public adjusters, contractors, and forensic accountants who can provide an unbiased and detailed evaluation of your property damage and business interruption losses. By gathering this objective evidence, your attorney builds a data-driven case that is much harder for the insurer to dispute. This step is critical for proving the full value of your claim and fighting back against a lowball offer.

Handle Negotiations, Appeals, and Lawsuits

Once your lawyer has analyzed your policy and gathered strong evidence, they take over all communication with the insurance company. You no longer have to deal with endless phone calls or pressure tactics from adjusters. Your attorney will present the evidence and handle all negotiations to secure a fair settlement. If the insurer refuses to cooperate or makes a lowball offer, your lawyer will manage the formal appeal process. And if negotiation fails, a seasoned trial lawyer is prepared to file a lawsuit and fight for you in court. This willingness to go to trial gives them significant leverage, as insurers often prefer to settle rather than face a skilled litigator.

What to Look for in a Commercial Insurance Claim Lawyer

Choosing the right lawyer can feel overwhelming, but it’s one of the most important decisions you’ll make for your business. You need more than just a legal representative; you need a strategic partner who understands what’s at stake. When your business is on the line, finding an attorney with the right combination of experience, skills, and client-focused practices is essential. Look for a lawyer who not only knows the law but also has a demonstrated history of standing up to insurance companies and winning. This isn’t the time to hire a generalist. You need a specialist who lives and breathes insurance disputes and has a deep understanding of the tactics insurers use to protect their profits.

The right attorney will do more than just file paperwork. They will build a comprehensive strategy tailored to your specific situation, bringing in their own experts to counter the insurance company’s assessments and fighting for every dollar you are owed. They act as your shield and your sword, handling all communications with the insurer so you can focus on running your business. Making the right choice from the start sets the tone for the entire dispute and significantly influences your chances of a successful outcome. To help you make an informed decision, focus on four key qualities during your search.

A Proven Record of Fighting Underpayment Cases

When you’re vetting attorneys, their track record should be at the top of your list. You want someone who has specific experience fighting and winning underpayment cases for businesses like yours. Ask potential lawyers about their past cases. How often do they handle commercial property claims? What were the outcomes? A lawyer with a history of turning lowball offers into fair settlements has the experience to anticipate an insurer’s tactics. You can often find case studies or a summary of past results on a firm’s website, giving you a clear picture of their ability to deliver for their clients. This proof is far more valuable than any promise.

Strong Negotiation and Trial Skills

The best commercial insurance lawyers are skilled negotiators who can often secure a fair settlement without ever stepping into a courtroom. However, they must also be fully prepared to take your case to trial if the insurance company refuses to be reasonable. An attorney with a reputation as a formidable trial lawyer sends a strong message to the insurer that you won’t back down. This dual threat of tough negotiation and trial readiness is your greatest leverage. Look for credentials like Board Certification in trial law, as it shows an attorney like Tim Hoch has achieved a verified level of expertise in the courtroom.

A Contingency Fee Agreement (So You Don’t Pay Upfront)

Your business is already facing financial strain from the underpaid claim, so the last thing you need is another hefty bill. That’s why you should look for a lawyer who works on a contingency fee basis. A contingency fee agreement means the lawyer only gets paid if they win your case, with their fee being a percentage of the final settlement or verdict. This arrangement aligns your interests with your lawyer’s, as they are directly motivated to recover the maximum amount possible for you. It also allows you to pursue justice without paying legal fees out of pocket.

Deep Knowledge of Texas Insurance Law

Insurance law varies significantly from state to state, so hiring a lawyer with deep expertise in Texas-specific regulations is non-negotiable. An attorney who specializes as a Fort Worth property insurance lawyer will understand the Texas Insurance Code, local court procedures, and the common tactics used by insurers operating in our state. This localized knowledge is critical for building a strong case, meeting important deadlines, and effectively countering the insurance company’s arguments. A local expert knows the landscape and can give you the home-field advantage you need.

What Does the Claims Dispute Process Look Like?

When your insurance company refuses to pay what they owe, you might wonder what happens next. The path to resolving a disputed claim isn’t always straightforward, but it generally involves a few key stages. Understanding this process helps you know what to expect and why having an experienced advocate on your side is so important from the very beginning.

The Role of Mediation and Negotiation

Often, the first step is trying to resolve the dispute through negotiation or mediation. Negotiation is a direct conversation between your lawyer and the insurance company to reach a settlement. Mediation is a bit more formal; the American Bar Association describes it as a process where a neutral third party helps both sides find common ground. Insurance companies sometimes prefer these methods because they can be faster and less expensive than a full-blown lawsuit. However, without a strong legal advocate, you risk accepting a lowball offer just to put the issue to rest. An experienced lawyer ensures your interests are protected during these critical discussions.

When a Lawsuit Becomes Necessary

If the insurance company still won’t offer a fair settlement through negotiation or mediation, filing a lawsuit may be the only way to hold them accountable. This step formally takes the dispute to court. While the thought of a lawsuit can be intimidating, it’s often the necessary leverage to make an insurer take your claim seriously. An attorney who is prepared to go to trial sends a powerful message that you will not back down. This is where having a lawyer with a proven track record of successful results in court becomes invaluable. They will handle the complex legal procedures, gather evidence, and build a compelling case to present before a judge or jury.

What You Can Expect to Recover

The goal of any claim dispute is to recover the full amount your business is owed. This can include money for property damage, repairs, replacement costs, and even lost income while your business was interrupted. The exact amount you can recover depends on your policy limits, the extent of your damages, and the strength of your case. The insurance company will look for any reason, from deductibles to policy exclusions, to reduce your payout. A dedicated property insurance lawyer works to counter these tactics, ensuring every loss is documented and accounted for to fight for the maximum compensation you deserve.

Protect Your Business Before You Even File a Claim

The best way to fight an underpaid claim is to build a strong case from the very beginning. While you can’t prevent a storm or accident, you can take steps right now to protect your business and put yourself in the best possible position for a fair payout. Think of it as setting the stage for success long before you ever have to make that call to your insurance company. This proactive approach isn’t just about good record-keeping; it’s about shifting the power dynamic. When you’re prepared, you’re not just reacting to what the insurance company tells you. Instead, you’re presenting a clear, evidence-backed account of your losses that they can’t easily dismiss.

A little preparation goes a long way. By being organized and proactive, you can counter many of the tactics insurers use to delay or reduce payments. These simple habits can make a huge difference, turning a potential months-long battle into a much smoother process. When you have your ducks in a row, it’s much harder for an adjuster to argue with the facts. The following steps are your playbook for getting ready before disaster strikes. Taking control of the process early on demonstrates that you are a serious business owner who expects to be treated fairly, and it lays the groundwork for a successful claim.

Know Your Policy Inside and Out

Your commercial insurance policy is a contract, and it’s one of the most important ones your business has. Before you ever need to file a claim, take the time to actually read it. I know, it’s not exactly light reading, but understanding what’s covered, what’s excluded, and what your responsibilities are is critical. Pay close attention to your coverage limits, deductibles, and any specific duties required of you after a loss. This knowledge is your first line of defense. When you understand the rules of the game, you’re better equipped to make sure your insurer plays by them, too. If the language feels confusing, having a Fort Worth property insurance lawyer review it can provide much-needed clarity.

Keep Detailed Records of Your Assets

If you had to create a list of every single item your business owns from memory, could you do it? Probably not. That’s why documenting your assets before you have a loss is so important. Create a detailed inventory of your equipment, furniture, supplies, and inventory. Take photos and videos of your property, both inside and out, and store them securely in the cloud. Keep receipts for major purchases and records of any upgrades you’ve made to the property. This creates a clear “before” picture that makes it much easier to prove the full extent of your “after.” This simple step provides the concrete evidence needed to support your claim and counter any attempts to downplay your losses.

Report Claims Promptly and Accurately

When damage occurs, your policy requires you to report it to the insurance company in a timely manner. Don’t delay. As soon as it’s safe, notify your insurer about the loss according to the procedures outlined in your policy. Failing to meet these deadlines can give them an easy reason to deny your claim. When you file, be honest and provide as much accurate detail as possible, but stick to the facts. You will also likely need to submit a sworn “proof of loss” form, which is a formal statement detailing the scope of your damaged property and its value. Meeting these deadlines is a crucial part of upholding your end of the insurance agreement.

How Hoch Law Firm Fights for Texas Business Owners

When your business suffers a loss, you expect your insurance company to make you whole. But when they come back with an offer that barely covers a fraction of your damages, it can feel like a second disaster. At Hoch Law Firm, we believe Texas business owners deserve to be treated fairly. We step in to hold insurance companies accountable and fight for the full compensation you need to recover.

Our approach starts with a deep dive into your commercial policy. These documents are often dense and confusing, but as experienced Fort Worth property insurance lawyers, our team knows exactly where to look for every bit of coverage you’re entitled to. We analyze the fine print to build a powerful case that counters the insurer’s lowball assessment. Led by Tim Hoch, a Board Certified trial lawyer, we have years of experience going head-to-head with large insurance corporations and winning.

We don’t just argue with the adjuster; we build an undeniable claim. This often means bringing in our own team of independent experts, like engineers, public adjusters, and contractors, to document the true scope and cost of your damages. We handle all communications with the insurance company, manage the complex appeals process, and prepare to take your case to court if that’s what it takes. Our proven results show our commitment to securing the funds our clients need to rebuild.

Throughout this entire process, our focus is on you. We know you need to concentrate on running your business, not fighting a legal battle. We keep you informed every step of the way and manage the heavy lifting so you can get back to what you do best. Because we work on a contingency fee basis, you won’t pay us any attorney’s fees unless we win your case. You don’t have to accept an insurer’s unfair decision, and you don’t have to fight them alone.

Related Articles

- When to Hire a Fort Worth Underpaid Commercial Claim Attorney

- McKinney Commercial Property Claim Lawyer: A 2026 Guide

- Business Interruption Claim Attorney Oklahoma: A Guide

- How a Denton Business Property Damage Lawyer Helps You

Frequently Asked Questions

I already cashed the insurance check. Is it too late to fight for more money? Not necessarily. Cashing a check from your insurer doesn’t automatically mean you’ve settled the entire claim, especially if you haven’t signed a final release document. In Texas, you can often file a supplemental claim if you discover the initial payment was not enough to cover the full cost of repairs. The key is to act quickly. An experienced attorney can review your specific situation and determine the best path forward for recovering the additional funds your business needs.

What’s the difference between hiring a public adjuster and an insurance claim lawyer? This is a great question. A public adjuster is an expert in assessing property damage and estimating repair costs, and they can be a huge asset in documenting your loss. However, their role stops there. An insurance claim lawyer can do everything a public adjuster does and more. They can interpret the complex legal language of your policy, formally dispute policy misinterpretations, and, most importantly, file a lawsuit and fight for you in court if the insurance company acts in bad faith or refuses to negotiate fairly.

My business needs repairs now. How long does the process of disputing a claim usually take? The timeline can vary quite a bit, and it really depends on how willing the insurance company is to be reasonable. A straightforward negotiation might be resolved in a few months, while a case that requires a lawsuit will naturally take longer. An experienced lawyer’s goal is always to resolve your claim as efficiently as possible. Often, just having a skilled attorney involved can speed things up because it shows the insurer you are serious about getting a fair result.

How much does it cost to hire a lawyer for this? My business is already struggling financially. This is a critical concern, and it’s why reputable commercial insurance lawyers work on a contingency fee basis. This means you pay no upfront costs or attorney’s fees. The law firm covers the expense of building your case, including hiring experts. Their fee is a percentage of the money they successfully recover for you. Simply put, if you don’t get paid, they don’t get paid. This approach allows you to access top-tier legal help without putting more financial strain on your business.

My claim was underpaid, but not by a huge amount. Is it still worth pursuing? Even a seemingly small underpayment can be a sign of a bigger problem and can leave you paying out of pocket for repairs. It’s always worth getting a professional opinion. A brief consultation with an insurance lawyer can help you understand the true value of your claim and whether the insurer’s offer was made in good faith. Since these lawyers work on contingency, they will give you an honest assessment of whether pursuing the case makes financial sense for both you and them.

For tailored guidance on a disputed or high-value claim, speak with a Fort Worth commercial insurance claim lawyer before important deadlines or evidence issues narrow your options.