Let’s be direct: your insurance company is not your partner. It’s a business designed to be profitable, and that profit comes from collecting your premiums while paying out as little as possible on claims. When your commercial property suffers a fire, this business reality becomes painfully clear. An insurer may use any reason, from a missed deadline to a fine-print policy exclusion, to justify a denial. For business owners in Texas, this can feel like a profound injustice. This guide pulls back the curtain on the insurance industry’s tactics. Understanding why and how they deny claims is the first step to building a powerful counter-strategy and knowing when to bring in a denied commercial fire claim lawyer to enforce your rights.

Key Takeaways

- Document Everything Immediately: Before you move or clean a single item, take extensive photos and videos of the damage. Keep a detailed log of every expense, get a copy of the fire report, and create a paper trail by confirming all verbal conversations with your insurer in writing.

- Understand Your Insurer’s Motives: Remember that your insurance company is a for-profit business, and its goal is to minimize payouts. Scrutinize their settlement offers, question low estimates, and never accept a verbal promise as a guarantee of coverage.

- Know When to Call for Backup: A claim denial is not the final word. If your insurer denies your claim without a solid reason, makes an unreasonably low offer, or uses significant delay tactics, it’s a clear sign to consult an experienced attorney who can fight for your rights.

Why Insurers Deny Commercial Fire Claims

After a fire, you expect your insurance company to step up and help you recover. Unfortunately, that’s not always what happens. Insurance companies are for-profit businesses, and their goal is often to pay out as little as possible. They may use complex policy language, strict deadlines, and intense investigations to find reasons to underpay or deny your claim entirely. It’s a frustrating reality for many Texas business owners who have faithfully paid their premiums for years.

Understanding the common reasons for denial is the first step in protecting your rights. Insurers might point to fine print in your policy, question the value of your losses, or even suggest you were somehow at fault. These tactics can feel overwhelming, especially when you’re trying to get your business back on its feet. Knowing what to expect can help you prepare a stronger claim from the start and recognize when the insurance company isn’t treating you fairly. This is where having an experienced Fort Worth property insurance lawyer can make all the difference, ensuring your claim is handled correctly and you are positioned to fight back against an unjust denial.

The Fine Print: Policy Exclusions and Gaps

Your commercial property insurance policy is a detailed contract filled with specific terms, conditions, and, most importantly, exclusions. An insurer might deny your claim by pointing to a clause that excludes damage from certain events. For example, if they determine the fire was caused by an issue specifically listed as uncovered, like a known electrical problem you failed to fix, they can refuse payment. They might also argue that you didn’t meet a condition of the policy, such as maintaining a functional fire alarm system. These policy details are often written in dense legal language, making it easy for business owners to misunderstand their actual coverage until it’s too late.

Missed Deadlines or Incomplete Paperwork

Insurance companies operate on strict timelines. Your policy will outline specific deadlines for reporting the fire and submitting your proof of loss. Missing one of these deadlines is one of the easiest ways for an insurer to deny your claim, regardless of its merit. The aftermath of a fire is chaotic, and it’s understandable that paperwork might not be your first priority. However, insurers are not always forgiving. They also require extensive and detailed documentation, and submitting an incomplete claim can lead to significant delays or an outright denial. It’s critical to follow all procedural requirements to the letter to protect your right to compensation.

Not Enough Proof of Your Losses

The responsibility to prove the full extent of your damages falls on you, not the insurance company. If you don’t provide sufficient evidence of what was lost and what it was worth, your insurer will likely undervalue your claim. This means you need to create a comprehensive inventory of all damaged property, from the building structure itself to equipment, furniture, and inventory. Simply stating your losses isn’t enough; you need to back it up with photos, videos, receipts, and professional estimates. Without thorough documentation, the insurer has the leverage to dispute the value of your claim and pay you far less than you need to rebuild.

Allegations of Negligence or Arson

One of the most serious reasons for a claim denial is an accusation of arson or gross negligence. If the insurance company’s investigation suggests the fire was intentionally set or that your extreme carelessness led to the blaze, they will deny the claim and may even report their findings to law enforcement. These are damaging allegations that can have consequences far beyond your insurance claim. An insurer might use any hint of financial trouble as a motive or misinterpret the cause of the fire. Fighting these accusations requires a strong, evidence-based response to defend your name and pursue the coverage you deserve for your business’s recovery.

Disagreements Over Repair Costs

Even when an insurer accepts liability, disputes often arise over the cost of repairs. The insurance adjuster’s estimate may come in significantly lower than the quotes you receive from local contractors. This is because adjusters may use cheaper materials, outdated pricing, or suggest repairing items that should be replaced entirely. Their job is to minimize the payout, not to ensure your property is restored to its pre-fire condition. You do not have to accept their lowball offer. You have the right to get your own independent estimates and negotiate for a fair settlement that truly covers the cost of rebuilding your business.

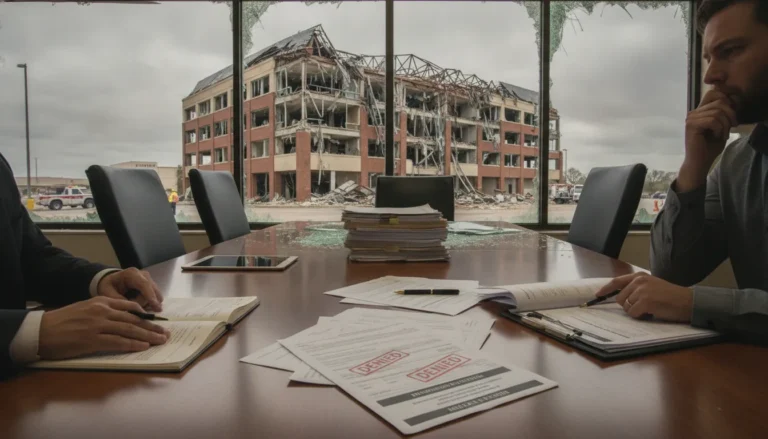

Your First Steps After a Commercial Fire

After the shock of a fire, the path forward can feel overwhelming. You’re dealing with damage, displacement, and the daunting task of getting your business back on its feet. The actions you take in the first few days and weeks are critical for the success of your insurance claim. While your first instinct might be to start cleaning up, it’s important to pause and approach the situation methodically. Think of this as gathering the essential tools and information you’ll need to rebuild.

Each step you complete builds a stronger foundation for your claim, making it harder for an insurance company to unfairly deny or underpay you. This process is about protecting your investment and your future. By documenting everything, understanding your coverage, and keeping meticulous records, you are taking control of the narrative. These initial actions can make a significant difference in your financial recovery and are fundamental to any property insurance dispute. Taking the time to get these steps right will serve you well throughout the entire claims process.

Take Photos and Videos of Everything

Before you move, clean, or throw anything away, document the scene thoroughly. Use your smartphone to take extensive photos and videos of all affected areas. Capture wide shots of rooms and close-ups of damaged equipment, inventory, and structural elements. Don’t forget to photograph soot and smoke damage on walls and ceilings, as well as any water damage from firefighting efforts. This visual evidence is one of the most powerful tools you have. It provides undeniable proof of your losses and helps you create a detailed inventory list later on, making it difficult for an adjuster to dispute the extent of the damage.

Find Your Policy and Read It

Your commercial property insurance policy is the rulebook for your claim. Locate your full policy documents, not just the declarations page, and read through them carefully. Every policy is different, so you need to understand exactly what your specific policy covers. Pay close attention to sections detailing coverage for the building itself, business personal property (like computers and machinery), and business interruption. This will tell you what you’re entitled to claim for repairs, replacements, and lost income while your business is closed. Knowing your policy’s terms, conditions, and limits is the first step to ensuring you receive everything you are owed.

Get Official Reports and Independent Estimates

Your documentation should go beyond your own photos. Request a copy of the official report from the fire department that responded to the incident. This report contains important details about the fire’s origin and cause. Next, contact several trusted, independent contractors to provide detailed repair and rebuilding estimates. Do not rely solely on the estimate from the contractor your insurance company sends. Having your own independent repair estimates gives you a realistic baseline for costs and provides powerful leverage when negotiating with your insurer, especially if their initial offer is too low.

Track Every Expense and Lost Income

From the moment the fire is out, start a detailed log of every single expense related to the damage. This includes the cost of boarding up windows, hiring a security service to protect the property, or renting temporary office space. Keep every receipt, no matter how small. At the same time, begin calculating your lost business income. Gather your past financial statements to project the revenue you are losing each day your business is non-operational. This meticulous financial documentation is vital for substantiating your claim for both extra expenses and business interruption coverage.

Put All Insurer Communications in Writing

While it’s common to speak with your insurance adjuster over the phone, never rely on verbal agreements. After every phone call, send a brief, polite email to the adjuster summarizing what was discussed, what they promised, and any deadlines they gave you. This simple step creates a written record of your conversations. This paper trail is invaluable if a dispute arises later or if the insurance company tries to deny that a certain agreement was made. It holds the insurer accountable and ensures everyone is on the same page throughout the claims process.

Never Miss a Policy Deadline

Insurance policies are filled with strict deadlines that you must meet to keep your claim in good standing. The most important one is often the deadline for submitting your sworn “Proof of Loss” form, which is a formal statement detailing the scope and value of your claim. Missing this or any other deadline can give the insurance company grounds to deny your claim outright, regardless of its merit. As soon as you file your claim, read your policy to identify all time-sensitive requirements and mark them on your calendar. Managing these details is a key part of handling all practice areas of insurance law.

Common Myths About Fire Insurance Claims

After a fire, it’s easy to get tripped up by common misunderstandings about the insurance claims process. Believing these myths can lead to a denied or underpaid claim, leaving you to cover devastating losses on your own. Let’s clear up a few of the most persistent and damaging myths so you can approach your claim with a clear understanding of the road ahead.

“My policy covers absolutely everything.”

It’s a comforting thought, but unfortunately, it’s not true. No insurance policy covers everything, as all commercial policies have specific limits and exclusions. While most cover building damage, business property, and lost income, they often leave out specific perils unless you’ve purchased extra coverage. It’s critical to read the fine print to understand what is and isn’t covered. A Fort Worth property insurance lawyer can help you interpret the complex language and identify any gaps before they become a problem.

“A verbal promise from my adjuster is good enough.”

An insurance adjuster might seem friendly, but a verbal conversation is not a binding contract. Never rely on spoken promises. If an adjuster tells you a repair will be covered, ask for it in writing. Your best practice is to document every interaction. After a phone call, send a follow-up email summarizing what was discussed and asking the adjuster to confirm its accuracy. This creates a paper trail that can be essential if a dispute arises later. Only official, written communication from the insurer holds any legal weight.

“The insurance company wants to be fair.”

While many adjusters are professionals, their employer is a for-profit business. This means they have a financial incentive to pay out as little as possible on claims. Insurers often delay, undervalue, and deny valid claims, knowing that many policyholders will get frustrated and give up. Believing the insurer is entirely on your side can cause you to accept a lowball offer. Our firm’s track record of results shows that challenging unfair offers is often necessary to get the payment you deserve.

“I can fight a denied claim by myself.”

As a business owner, you’re used to solving problems, but battling a major insurance company is a different kind of fight. Insurers have vast resources and deep experience in finding reasons to deny claims. Going it alone puts you at a significant disadvantage. An experienced attorney understands these tactics and knows how to counter them. Tim Hoch, a Board Certified trial lawyer, can analyze your policy, gather evidence, and handle all negotiations. This levels the playing field and gives you the best chance at a successful outcome.

What Are Your Legal Options for Bad Faith?

When your insurance company denies your fire claim without a reasonable basis, it might be more than just a disagreement. It could be an act of bad faith. This means the insurer isn’t just wrong; they are unfairly and intentionally avoiding their legal duty to you. As a policyholder in Texas, you have specific rights and several powerful options to fight back and hold them accountable.

Spotting Bad Faith Insurance Tactics

An insurer acts in bad faith when it denies a claim without a good reason and knows it, or simply doesn’t bother to find out. It’s a deliberate attempt to protect their profits at your expense. While a legitimate dispute over costs isn’t automatically bad faith, a pattern of dishonest behavior often is.

Common red flags include:

- Unreasonably delaying the investigation or payment of your claim.

- Offering you far less than your claim is worth without a clear explanation.

- Misrepresenting what your policy covers.

- Refusing to provide a reason for the denial in writing.

- Failing to conduct a complete and fair investigation.

If these tactics sound familiar, it’s time to consider that your insurer isn’t playing by the rules. A Fort Worth property insurance lawyer can help you determine if the insurer’s actions constitute bad faith.

Mediation, Arbitration, and Taking Legal Action

After a denial, you have a choice. You can give up, which is exactly what the insurance company hopes you’ll do. Or, you can hire a lawyer to make the insurance company pay what they owe. An experienced attorney can guide you through several paths. Mediation involves a neutral third party who helps you and the insurer negotiate a settlement. Arbitration is more formal, where an arbitrator hears both sides and makes a decision that is often binding.

If negotiation fails, filing a lawsuit may be the necessary next step to enforce your rights. Taking legal action sends a clear message that you will not accept an unfair denial. Exploring your legal options is the first step toward getting the resolution you deserve.

Filing a Complaint with Texas Regulators

Another tool at your disposal is filing a formal complaint with the Texas Department of Insurance (TDI). The TDI is the state agency responsible for regulating insurance companies. They investigate consumer complaints and can penalize insurers for violating state laws, including engaging in bad faith practices.

Filing a complaint creates an official record of the insurer’s misconduct and can put pressure on them to reconsider your claim. However, keep in mind that the TDI’s primary role is enforcement, not compelling payment for your individual claim. While it’s a valuable step, it often works best in conjunction with legal action, not as a replacement for it.

What Damages You Can Potentially Recover

A successful bad faith lawsuit can help you recover much more than just the original amount of your fire damage claim. Texas law allows policyholders to seek additional compensation when an insurer has acted unfairly. If you win your case, you may be able to recover:

- The full benefits owed to you under your insurance policy.

- Interest on the delayed payments (up to 18% in Texas).

- Compensation for your attorney’s fees.

- In some cases, punitive damages, which are intended to punish the insurer for their wrongful conduct and deter them from doing it again.

These potential results show that fighting back isn’t just about getting what you were initially owed; it’s about holding the insurer fully accountable for the harm their actions caused.

How a Denied Fire Claim Lawyer Helps You

When an insurance company denies your fire claim, it can feel like you’ve hit a wall. You’ve paid your premiums faithfully, and now the support you counted on isn’t there. This is where a lawyer can step in and make a real difference. Instead of you trying to decipher complex legal documents and argue with seasoned adjusters, an experienced attorney takes on that burden. They become your advocate, using their legal knowledge to challenge the denial and fight for the compensation your business needs to recover.

Analyzing Your Policy and Denial Letter

The first thing a skilled attorney will do is a deep-dive review of your insurance policy and the denial letter. Commercial insurance policies are dense, complicated documents filled with specific terms, conditions, and exclusions. Your lawyer will examine every line to understand exactly what your policy covers and identify the insurer’s stated reason for the denial. They can pinpoint weak arguments or misinterpretations the insurance company might be using to avoid payment. A property insurance lawyer understands the nuances of Texas insurance law and can determine if the insurer’s position is legally sound or if they are acting in bad faith.

Building a Strong Case with Evidence

A denial is often just the start of the conversation, but you need powerful evidence to change the outcome. An attorney helps you gather and organize everything needed to build a compelling case. This goes beyond just taking photos of the damage. They will help you document everything methodically, from creating a detailed inventory of lost business property to tracking lost income and extra expenses incurred during the disruption. Your lawyer may also bring in independent experts, like structural engineers or public adjusters, to provide a comprehensive and unbiased assessment of your losses. This ensures your claim is not just a number but a fully supported demand for what you are rightfully owed.

Handling All Negotiations with the Insurer

Dealing with an insurance company after a denial can be incredibly frustrating. Adjusters are trained negotiators whose goal is often to pay as little as possible. When you hire an attorney, they take over all communications and negotiations on your behalf. This immediately levels the playing field. Your lawyer will present the evidence, make legal arguments, and counter any lowball settlement offers. Having a seasoned trial lawyer like Tim Hoch in your corner sends a clear message to the insurer that you are serious about getting a fair outcome and won’t be pushed around by delay tactics. This allows you to focus on rebuilding your business while your lawyer handles the fight.

Taking Your Fight to Court

If the insurance company refuses to negotiate fairly and offer a reasonable settlement, your lawyer won’t back down. A trial attorney is always prepared to take your case to court. Filing a lawsuit can be the necessary step to hold an insurer accountable for their obligations. While many cases settle before a trial, the willingness and ability to litigate your claim is a powerful tool. It shows the insurance company that you have the resources and determination to see the fight through to the end. Seeing a firm’s past results can give you confidence that your case is in capable hands, whether it’s resolved through negotiation or in a courtroom.

What a Successful Appeal Can Achieve

When your commercial fire claim is denied, it can feel like you’ve hit a dead end. But a denial is not the final word. Pursuing an appeal with the right legal support can do more than just reverse the insurance company’s decision; it can lead to the full and fair compensation you deserve for your losses. A successful appeal holds your insurer accountable and helps you get your business back on its feet.

Overturning the Denial for Full Payment

The primary goal of an appeal is to get the insurance company’s denial overturned and secure payment for your claim. A denial often happens because the insurer claims your situation falls under a policy exclusion or that you didn’t provide enough proof. An experienced property insurance lawyer can challenge these reasons by conducting a thorough review of your policy and the fire’s circumstances. They will help you gather the necessary evidence, from expert reports to financial documents, to build a strong case that clearly demonstrates why your claim should be paid in full. A well-prepared appeal leaves no room for the insurer to misinterpret the facts or their obligations.

Negotiating a Fair Settlement

Even if an insurer agrees to reverse a denial, their initial settlement offer may be far less than what you need to truly recover. Insurers are businesses, and their goal is often to pay out as little as possible. This is where negotiation becomes critical. An attorney who understands the complexities of commercial property policies can advocate on your behalf to ensure you receive what you are entitled to. They will fight for a fair payment that covers not just the structural repairs but also lost business income, damaged equipment, and other costs you’ve incurred. Their experience allows them to counter lowball offers and push for a settlement that reflects your actual losses.

Recovering Damages for Bad Faith Conduct

Sometimes, an insurer’s denial isn’t just a disagreement; it’s a result of them acting in bad faith. This can include denying a claim without a reasonable investigation, intentionally misinterpreting policy language, or creating unnecessary delays. If your insurer is found to have acted in bad faith, you may be able to recover more than just the money owed under your policy. Texas law allows policyholders to seek additional damages for this misconduct. A successful bad faith claim could mean you recover compensation for interest on the delayed payment, and in some cases, the court may even require the insurance company to pay your attorney’s fees.

When to Hire a Lawyer for Your Denied Claim

After a fire, a denied claim can feel like a second disaster. You might wonder if it’s worth the fight or if you should just accept the insurance company’s decision. While you can handle minor disagreements on your own, certain situations are clear signs that you need professional legal help to protect your business. Knowing when to call in an expert can be the difference between closing your doors for good and rebuilding stronger than before.

Red Flags That You Need Legal Support

Trust your gut. If something feels off about how the insurance company is handling your claim, it probably is. A major red flag is when your claim is denied without a clear, valid reason that is explicitly stated in your policy. Another is a settlement offer that is obviously too low to cover your actual losses. Don’t let an insurer pressure you into accepting a fraction of what you’re owed. Finally, pay attention to unreasonable delays. If the company is dragging its feet for months without a decision or payment, they may be hoping you’ll just give up. These tactics are often signs of bad faith, and it’s time to explore your legal options.

How Contingency Fees Work

Many business owners hesitate to hire a lawyer because they worry about the cost, especially when they’ve just lost so much. This is where a contingency fee arrangement can be a lifeline. In simple terms, it means you don’t pay any attorney’s fees unless your lawyer successfully recovers money for you. The firm’s payment is a pre-agreed percentage of the final settlement or court award. This structure ensures your lawyer is just as motivated as you are to get the best possible outcome. It removes the upfront financial risk and allows you to access top-tier legal representation when you need it most.

Finding the Right Attorney in Texas

When your business is on the line, you need more than just any lawyer; you need an advocate. Look for an attorney who has specific experience with commercial property insurance disputes in Texas and who exclusively represents policyholders, not insurance companies. A skilled property insurance lawyer will thoroughly analyze your policy, gather the right evidence to build a strong case, and handle all communications with the insurer. You want a seasoned trial lawyer who isn’t afraid to take your case to court if a fair settlement can’t be reached. An attorney like Tim Hoch, who is Board Certified in Personal Injury Trial Law, brings a level of expertise that can make all the difference.

Related Articles

- Fort Worth Commercial Fire Damage Attorney: Maximize Your Claim

- Why Hire a Contingency Lawyer for Commercial Fire Claim?

- Why Hire a Law Firm for a Business Interruption Claim

- McKinney Commercial Property Claim Lawyer: A 2026 Guide

- 5 Ways an Apartment Fire Attorney Can Help

Frequently Asked Questions

My insurer’s repair estimate is way lower than my contractor’s. What should I do? This is a very common situation, so don’t feel discouraged. You are not required to accept the insurance company’s low estimate. Their adjusters often use standardized pricing or suggest patch-up jobs that don’t fully restore your property’s value. Your next step should be to get detailed, written estimates from two or three trusted, independent contractors in your area. These independent quotes provide a realistic picture of local labor and material costs and serve as powerful evidence when negotiating for a fair settlement that truly covers the cost of rebuilding.

How do I know if my insurer is acting in bad faith or if we just disagree? A simple disagreement over the value of a specific item is not usually bad faith. Bad faith involves a pattern of unreasonable and unfair conduct. Ask yourself if the insurer is refusing to provide a written reason for its denial, creating extreme and unexplained delays, or misrepresenting what your policy says. If you see a trend of dishonest behavior or feel the company is intentionally creating roadblocks without a valid cause, it may be more than a simple dispute. It could be a sign they are not upholding their legal duty to you.

I’m worried about the cost. How can I afford a lawyer after my business has been damaged by a fire? This is a completely valid concern, and it’s one that prevents many business owners from getting the help they need. Most reputable property insurance lawyers handle these cases on a contingency fee basis. This means you do not pay any attorney’s fees upfront. The lawyer’s fee is a percentage of the money they successfully recover for you. If they don’t win your case, you don’t owe them a fee. This approach allows you to get expert legal help without any out-of-pocket financial risk.

The insurance adjuster seems friendly. Can’t I just negotiate a settlement with them on my own? While an adjuster might be personable, it’s important to remember their job is to protect the insurance company’s financial interests, not yours. They are trained negotiators who handle claims like yours every day. Negotiating on your own puts you at a significant disadvantage because you are not on a level playing field. An experienced attorney understands the insurer’s tactics, knows the legal arguments to make, and can handle all the stressful back-and-forth, ensuring you are not pressured into accepting an unfair offer.

I think I might have missed a policy deadline. Is my claim automatically lost? Missing a deadline, especially for submitting your formal proof of loss, is serious and can be a reason for an insurer to deny your claim. However, it doesn’t always mean your claim is automatically defeated. An attorney can review the specific circumstances, your policy’s language, and all communications with the insurer to determine if there are still options available. The key is to not delay any further. Seeking a legal opinion right away is the best way to understand if you can still fight the denial.